client log-in

client log-in

Fireside Chat: Plug Power (PLUG) CSO Sanjay Shrestha – Thursday Feb. 11th @ 11am

For access information, email us at [email protected]

W|EPC: Commonwealth LNG Project Update, Comps, & Due Diligence Questions Q121

View This Report In Our Webstore

For access information please email us at [email protected]

Read More

***Conference Call: Alternative Fuels – Emissions, Feedstock, & Gas Stations, Thurs 2/4 @ 2PM EST – Future Of Transport (Part 3)***

Hydrogen Roadmap – Fuel Comparisons: Emissions, Feedstock, & Gas Stations – Future Of Transportation (Part 3)

For access information, email us at [email protected], or at [email protected]

Read More

S&P Global | PLATTS: US LNG Exporters Keep Utilization Near Capacity As Asia Prices Test New Heights

Read More

W|EPC: Mozambique LNG – Baseline Report & On-Site Satellite Image Analysis (Q121)

Mozambique LNG – Q121

Baseline Report & On-Site Satellite Image Analysis

Project Owners: Total, Mitsui, ENH, PTT, etc.

LNG Buyers: Tokyo Gas, JERA, Centrica, Shell, CNOOC, EDF, etc

For access information please contact us at [email protected]

Key Takeaways:

Mozambique LNG (MZLNG): After A Sluggish Start…The Next 6 Months Are Critical.

• Q320 & Q420 satellite images indications… (pgs. 15-18)

• 17-months after FID, meaningful piling, concrete, &/or structural steel erection [redacted]…

• Recent security issues (increasingly localized terrorism) could further hamper staffing levels and complicate the path forward (while also potentially creating the pretense for Force Majeure relief).

Schedule Analysis & Estimates: W|EPC Estimate MZLNG is…

• Our proprietary risk model implies a probability of the project meeting its original cost/schedule metrics is [redacted] (page 5)

• EPC Contract Exposure: ~$8B LSTK contract, via a consortium comprised of Saipem (74.95%, SAPMF), McDermott (24.98), MDR) & Chiyoda (0.07%,)

• Note: a successful project would boost Saipem’s reputation, while also certainly meaningful for a restructured MDR ($560MM Raise on Jan 5, 2021).

Mozambique vs. LNG Canada

• MZLNG & LNG Canada share similar characteristics, specifically: a remote area, greenfield, man-camp, etc. (page 4)

• Key differences: MZLNG’s has lower-cost construction wages, shorter project schedule, but 300% more peak labor (~11k craft workers).

• Should MZLNG require even more labor given the circumstances described in pages that follow, it would likely require an even more significant pull from local labor (on-site housing can support ~9.5k workers).

• MZLNG is located in one of the least developed areas of Mozambique, which creates unique risks around that heavy lean on local labor, even before considering the uptick in localized terrorism. (page 12)

Mozambique LNG: Baseline Report Q121

Mozambique LNG: Baseline Report Q121 (Page 15)

W|EPC: Mozambique LNG – Baseline Report & On-Site Satellite Image Analysis (Q121)

For access information, please email us at [email protected], or reach out to Webber Research Institutional Sales at [email protected]

Read More

Webber Research: Hydrogen Roadmap Part 2 – Future of Vehicle Transportation Alternative Fuels – Efficiency & Safety

For access information, please contact us at [email protected] or at [email protected]

![]()

Read More

Conference Call: Future Of Vehicle Transportation – Alternative Fuels Efficiency & Safety w/ Baker Risk, 12/17 @2PM

![]()

Conference Call: Fireside Chat With Enersys (ENS) CFO Mike Schmidtlein – Thursday 12/17 @ 11AM

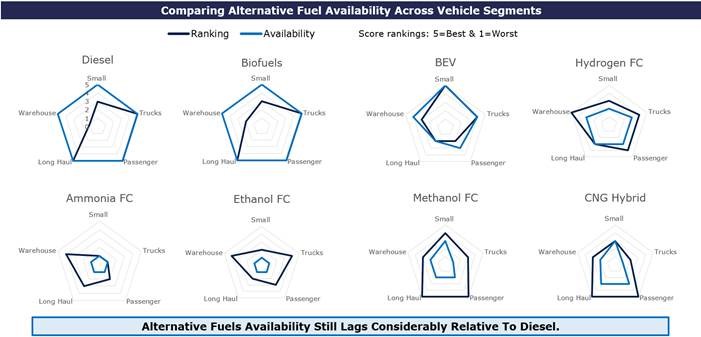

Client Conference Call: Ranking & Evaluating Alternative Fuels – The Future Of Vehicle Transportation H2 • BEV • Methanol • CNG Hybrid • Ethanol • Ammonia • Biofuels • Diesel

![]()

W|EPC: Future Of Transportation – Ranking & Evaluating Alternative Fuels – H2 ∙ BEV ∙ Methanol ∙ CNG Hybrid ∙ Ethanol ∙ Ammonia ∙ Diesel ∙ Biofuels

If you’re a current Webber Research subscriber you access this presentation via our Client Login above. If you’re not yet a subscriber, please contact us at [email protected] for access information.

Alternative Fuel Analysis…Will History Repeat Itself?

In 1992 & 2005, the Department of Energy (DOE) created & amended the Energy Policy Act (EPA) that addressed fuel research and tax benefits for vehicle manufacturing.

Battery Electric Vehicles (BEV), Hydrogen (H2), Hybrids, Biofuels, Ethanol and Methanol were analyzed in 2005, but vehicle manufacturers supported gasoline hybrid vehicles due to technology and production constraints.

Since then, fuel cell technology and global, federal, & state emission guidelines have accelerated innovation and the market is now actively deciding transportation alternatives.

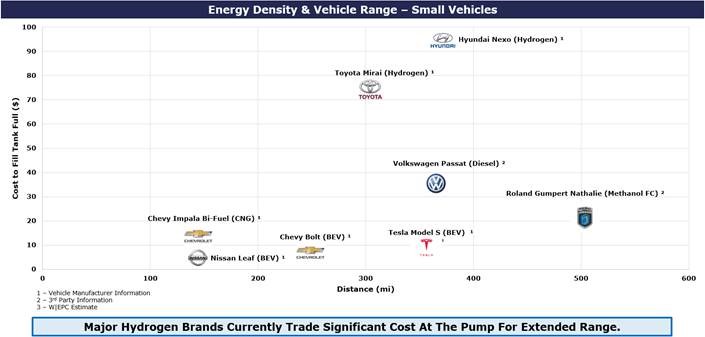

Small Vehicle Applications

BEV have taken a leading role in the small vehicle category with minimal competition from Hydrogen.

Hydrogen’s price, lack of infrastructure, and safety concerns highlight the risk associated with new fuel applications; however, Methanol may have an opportunity to fill this role.

The Roland Gumpert Nathalie markets an impressive range and methanol costs are comparative to BEV, but the $450k price tag limits it’s applications until manufacturing scales up to reduce cost.

Mid-Sized Vehicles and Truck Applications

Mid-Sized Vehicles and Truck Applications

Fuel energy density becomes a larger role as the size of a vehicle increases.

Fuel storage capacity, energy density, and vehicle efficiency play a large role in the range and cost for a vehicle.

Semi-Truck Range Is A Gating Issue For Future Fuels

New Semi-Truck concepts are ranging from shorter applications (<300 miles) to the long-haul market (>600 mile/day).

Daimler eCascadia seems to make sense for shorter applications and Hyliion’s Compressed Natural Gas (CNG) hybrid semi will likely apply well to long haul trades, if the marketing is as good as advertised.

Read More

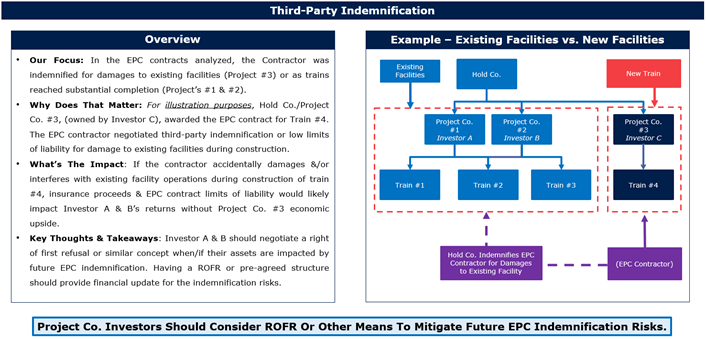

W|EPC: Analyzing Energy Project Contract Terms – Risks, Strategies & Comps

Analyzing Energy Project Contract Terms – Part 1 – Risks, Strategies & Comps Across Stakeholder Groups – Q420

Analyzing EPC Risk Avoidance: Comps & Techniques For Investors, Owners, & Contractors

W|EPC analyzed ~$20B of publicly available EPC lump sum turn-key (LSTK) contracts, focusing on sensitive or contentious terms used to allocate risk, manage performance expectations, & establish a framework for third-party indemnification and liquidated damages, etc. (Pages 3, 5-7, & 9-17). Specific points of emphasis:

- Investors: Leveraging a project’s future expansion plans to protect ROE and/ maximize options (ROFR) options. (Pages 5, 9-11)

- Owners: Finding & justifying onerous contract terms as market or on-the-run.

- Contractors: Avoiding those onerous contract terms.

Analyzing Notable Risks

- Liability & Indemnity: Existing Facilities can be problematic for Contractors & expose stakeholders. (Pages 5, 9-11)

- Performance Guarantees & Damages: Numerous performance guarantees were publicly disclosed (likely inadvertently) that illustrates risks & production, emissions, and/or power consumption liabilities. (Pages 6, 12-14)

- Technical Risk Allocation: One project’s subsurface provisions are tighter and limit change orders provisions for differences in soils data. (Pages 7, 15-17)

Distributing Project Risk Amid A Ramp In Renewables

- The steep ramp in renewables demand & project development could create an opportunity/leverage for participating EPC providers to ultimately own less project risk.

- Certain renewable projects could struggle getting an EPC LSTK contract (typically advantageous for the project owner, at the expense of the EPC provider). Dominion Energy (D), for instance, was unsuccessful in finding an EPC provider to provide a LSTK contract for their Coastal Virginia Offshore Wind (CVOW) project.

- EPC providers may have some leverage here, at least for now. W|EPC believes integrating EPC contract strategies/terms earlier than traditional projects (i.e. hydrocarbons) will improve risk/reward.

W|EPC: Analyzing Energy Project Contract Terms – Risks, Strategies & Comps

Table Of Contents:

- Key Takeaways – Page 2

- EPC Contracts Analyzed – Page 3

- Overview – Notable Risks for Any Projects – Page 4

- Third-Party Indemnification – Page 5

- Performance Guarantees – Page 6

- Rely-Upon Information – Page 7

- Contract Analysis, Significance, Negotiation Strategies, & Comps – Page 8

- Third-Party Indemnification – Page 9

- Performance Guarantees – Page 12

- Technical Risk Allocation – Page 15

For full access information, email us at [email protected], or at [email protected]

Read More

Webber Research: Reviewing California’s Rollout Plans For A Hydrogen Fueling Network

Webber Research: Reviewing California’s Rollout Plans For A Hydrogen Fueling Network Evaluating Safety, Cost, & Implementation Data

For full access information, email us at [email protected], or at [email protected]

In mid-November the California Air Resources Board (CARB) published initial plans detailing the development and implementation of a light-duty hydrogen fueling station networks, including a focus on financial self-sufficiency.

Specifically, CARB’s initial draft highlights:

1. Estimates around required state-support and eventual self-sufficiency

2. A comparison of existing market solutions, ongoing government research, and the latest awards in the Energy Commission’s Grant Funding program.

3. The economic sensitivity around FCEV deployment and the pace of network development.

4. Opportunities for cost reductions

5. Potential price reductions at the pump

6. Regional economic differences

Within the context of CARB’s report, we evaluated the economics and risks for deployment of Hydrogen fueling station options based on the following:

• Public Safety

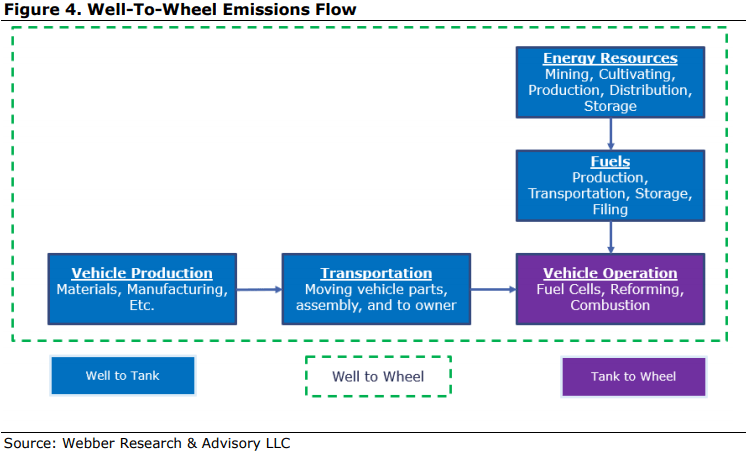

• Climate Change and Air Quality – Tank to Wheel (TTW) – Well to Wheel (WTW)

• Gas Station Infrastructure Costs

• Hydrogen Costs at Pump for Consumer

W|EPC Takeaway: As highlighted below, if the primary goal of CARB is to reduce tailpipe emissions, we believe electric vehicles and hydrogen vehicles are the most viable options today. However, if the goal is to reduce total emissions and to implement hydrogen fueling as quickly, safely, and cost-effectively as possible, it opens the door for a mix of other fuel considerations – including biofuels, e-fuels, and other energy mediums to expedite the Hydrogen Economy. We believe how California ultimately balances those priorities will determine what it’s future fueling network looks like.

Climate Change & Air Quality

Air quality and the need for sustainable future fuels to reduce GHG emissions is driving alternative fuel technology development. CARB’s Low Carbon Fuel Credits (LCFC) are based on Well to Wheel Carbon Intensity Scores (CI) that identify upstream pollution caused by fuels.

Gas Station Infrastructure Costs

Future fuels (i.e. H2, Ammonia, Methanol) will require new infrastructure in almost all cases to meet federal and state emission guidelines. The Implementation cost of these can vary from storage retrofitting, to +$1 million infrastructure upgrades. The costs could further increase based on the engineering design and blast radius study results.

Hydrogen gas station equipment could include:

• Compressors – 350 bar pressure

• Above Ground Storage

250 bar pressure

250 kg storage

• H2 Dispenser Larger corporate gas stations may have the financial means to implement the costly infrastructure upgrades especially if supported by fuel tax credits. However, smaller gas stations may face challenges investing in the capital costs & the ~$2K/month electricity bill to own & operate the equipment.

Cost comparisons vs the low-cost alternative for Methanol:

• Hydrogen – See Figure 6. Multiple scenarios based on CARB capital cost estimates

• Methanol to Hydrogen in Vehicle – ~$50,000 per gas station to upgrade storage

• Methanol to Hydrogen at Pump – ~$1 million per gas station (250kg H2 storage)

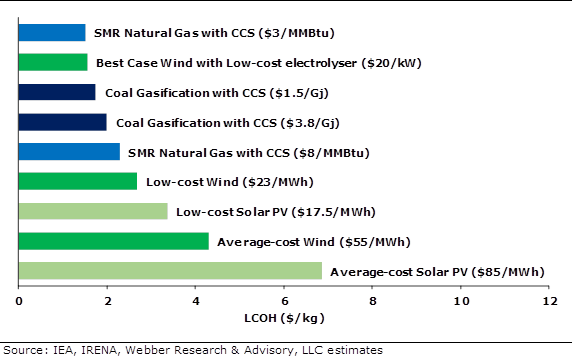

Hydrogen Costs at Pump for Consumer: ~$16/kg and by 2030 as Low as $8/kg?

At the pump, the H2 price begins to stack up due to CAPEX, maintenance, safety, and production costs. We have provided a few options that have been considered for comparisons sake below that could further drive down the cost of hydrogen.

• Centralized Electrolysis: ~$8/kg

• Centralized Reformer (No Carbon Capture): ~$2.50/kg

• Methanol Reforming at Pump: ~$5/kg

Includes 250kg hydrogen storage and compression

• Methanol Reforming in Vehicle: ~$3.50/kg

Gas Station infrastructure cost are relatively minimal

For a methanol reforming at pump scenario, storage-related infrastructure costs could be lighter as Methanol is a potential mid-stream solution for hydrogen, and is generally easier to store in large quantities – potentially pushing the hydrogen cost at the pump level below $10/kg in a shorter timeframe.

For full access information, email us at [email protected], or at [email protected]

Read More

W|EPC: Enterprise (EPD) PDH-2 Q420 Project Monitor & Satellite Image Review

Key Takeaways: Enterprise (EPD) PDH-2 Q420 Project Monitor & Satellite Image Review

EPD PDH 2 – Project Delay Analysis. In Q220, EPD announced a 3-month schedule slip (from Q123 to Q223), potentially limiting future change orders (i.e. cost escalation) related to COVID impact (based on typical EPC contract FM concepts).To reduce the COVID delay to only 3 months, we believe EPD implemented a schedule recovery plan that accelerated/compressed back-end construction activities to meet a Q423 COD forecast. (pgs. 10 – 13). We’ve independently estimated PDH 2’s slippage based on Q420 aerial project site images, with details found within our note… (pages 4 – 7).

Enterprise’s First ESG Guidance… : On October 28, 2020, EPD released their approach to ESG. In the report, EPD touts they are the largest Midstream producer of Hydrogen. With the addition of PDH2, Enterprise would increase their Hydrogen production by 140k tons/year, and we estimate ~150MW of electricity by incorporating fuel cells in their Mont Belvieu, TX facility.

Companies like SK are working with fuel cell manufacturers to integrate high temperature Solid Oxide Fuel Cells (SOFC) into PDH units to use the hydrogen produced to reduce operating costs….this could help EPD’s ESG potential.

Project Timeline Catch Up – Risks & Benefits: A schedule recovery plan can be costly and is not guaranteed to succeed. PDH 2 schedule recovery risks/benefits include: Risks – An EPC lump sum contractor (S&B) compresses the schedule & may cause inefficient construction & cost escalation. Benefits – The COVID delay started before site prep and avoided a de-staffing of the project. Based on limited on-site progress, S&B likely hasn’t spent much of their field budget & may have available contingency to support acceleration costs/inefficiencies.

W|EPC’s estimated timeline shows site labor and progress can support pulling activities back to Q223 with a probability of success of…. (pgs. 10-13)

W|EPC: Enterprise (EPD) PDH-2 Q420 Project Monitor & Satellite Image Review

For access information, please email us at [email protected], or our institutional sales at [email protected]

Read More

Webber Research: Renewables Weekly

Webber Research: Renewables Weekly 11/18/2020

- Highlights:

• PLUG – $846MM Public Offering

• ENPH ACM Partnership & Dist Agreement In The Philippines

• BLNK Cable Management Solution

• AMRC Completes Two Projects

• FLR Collaboration With Sargent & Lundy On Modular Nuclear Plant

• RIDE Business Updates

• Vestas Orders In Poland & UK

• SGRE Introduces Low-Wind Turbine

• Nordex 302MW Order In Texas

• DNV GL Certifies GE’s Haliade-X Prototype

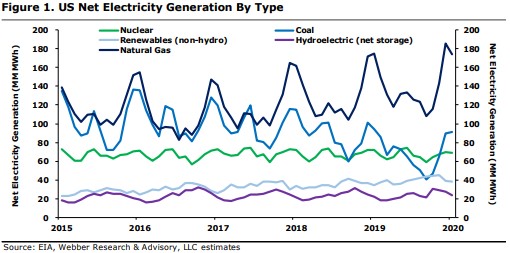

• US Net Electricity Generation

• Solar PV Pricing

• LCOE Benchmarks & Timeseries

• Global Wind Turbine Market Share

• Global Solar PV Inverter Market Share

• US Wind & Solar Projects Announced Or In Early Development - PLUG $846MM Public Offering: On 11/16 PLUG announced it would offer 38MM shares at $22.25 (11% discount to its previous close) for total proceeds of ~$846MM (upsized from $750MM). We note this is PLUG’s third public offering in the past year and adds to its $200MM convertible notes from May. PLUG ended Q3 with ~$450MM in unrestricted cash (+$700MM including restricted cash) which, even with significant Capex going to construction of the Gigafactory, we think was enough runway to 2023-2024 when PLUG is expected to start generating positive cash flow. The offering would bring PLUG’s pro forma cash balance to over $1.5B, which we think has less to do with added conservatism (after reporting positive Q3 EBITDA and raising its 2021 gross billings guidance last week) and more to do with accelerating its green hydrogen strategy, potential M&A, and/or other unannounced growth opportunities (partnerships in the US with a major software player or in the EU with an auto OEM). We’ll see…

- ENPH ACM Partnership & Distribution Agreement In The Philippines: On 11/16 ENPH announced an agreement with MSpectrum to distribute ENPH products to residential and commercial installers across the Philippines. IQ 7 products will be available in Q121. ENPH also announced a strategic partnership with DMEGC Solar Energy to develop a high-efficiency Enphase Energized AC Module (ACM) for the European solar market. The Mono PERC Black Enphase Energized ACM features IQ 7 microinverters and is currently available in France and the Netherlands.

- BLNK Cable Management Solution: On 11/16, BLNK introduced its new Cable Management Solution for new and existing EV Charger locations. The new system is compatible with rectangular and triangular pedestal charging stations as well as wall or pedestal mounted chargers. It also features a retraction mechanism similar to most gas pump designs for customer familiarity.

…continued

For access information, email us at [email protected], or go to webberresearch.com/downloads

Read More

Webber Research Expands Renewables & Energy Infrastructure Platform with Additions In New York & Houston

Read More

Webber Research: Renewables Weekly

Webber Research: Renewables Weekly 11/05/2020

- Baker Hughes (BKR) Buys Carbon Capture Platform

- Dominion (D )Proposes 9 New Solar Facilities For ~500MW

- AMRC – 2 New Contracts In Oregon

- Neste Acquires Neighboring Refinery Plant

- ITRI Deploys AMI In Canada

- AGR Investor Day & PNM Merger

- Vestas Buys Out MHI Stake In MHI Vestas JV

- AEP PPAs In Ohio

- Diamond Green Diesel Receives Air Permit From TCEQ

- US Net Electricity Generation

- Solar PV Pricing

- LCOE Benchmarks & Timeseries

- Global Wind Turbine Market Share

- Global Solar PV Inverter Market Share

- US Wind & Solar Projects Announced Or In Early Development

BKR Buys Carbon Capture Platform: On 11/3 BKR announced it acquired Compact Carbon Capture (3C) for an undisclosed amount. BKR plans to accelerate development and commercialization of 3C’s carbon capture solution, which adds to its existing portfolio of carbon capture technology including turbomachinery, solvent-based capture processes, well construction, CO2 storage management, and digital monitoring solutions…

Dominion Proposes 9 New Solar Facilities For ~500MW: On 11/2, Dominion Energy (D) proposed a slate of 9 new solar projects with output of 498MW. Six of the facilities (416MW) are through PPAs, helping to fulfill the Virginia Clean Economy Act (VCEA) requirement of having 1/3 of new solar and onshore wind be procured through PPAs through 2035….

AMRC 2 New Contracts In Oregon: On 10/26 and 10/27 AMRC…..

For access information, email us at [email protected], or go to webberresearch.com/downloads

Read More

Webber Research Recognized By Institutional Investor, Only New Firm To Rank Within 2020 US Equity Research Survey

Read MoreWebber Research Call Series – Monday, October 26th – Vogtle Nuclear Project Monitor – Key Decisions That Could Haunt Cost Prudency

Please join us for the latest Webber Research Client Call on Monday, 10/26 at 12PM, when we’ll discuss our latest deep dive into Southern Company’s Vogtle Nuclear expansion.

For access information, please contact us at [email protected], or our Institutional Sales Desk at [email protected]

![]()

W|EPC: Southern Company (SO) – Q420 Vogtle Project Monitor – Key Decisions That Could Haunt Cost PrudencyRead More

W|EPC: Southern Company (SO) – Q420 Vogtle Project Monitor – Key Decisions That Could Haunt Cost Prudency

Key Takeaways: Vogtle Q420 Monitor – Key Decisions That Could Haunt Cost Prudency

Who Will Be Getting Stuck With +$2.1B In Cost Overruns? Once Vogtle Unit 4 reaches “fuel load”, Georgia Power/Southern Company (GP/SO) can request a cost prudency determination to push their portion of cost overruns (~$2.1B) into recoverable utility rates. (Page 4)

Regulators will determine cost prudency based on project data, testimony, and a simple question: What should a reasonable manager have done at the time of the decision? (Page 5)

We expect that process to be heavily scrutinized considering the scale of the overruns, and, in our opinion, some questionable GP/SO decisions. (Pages 4-5)

Decisions That Could Haunt GP/SO’s Prudency. We believe there’s a case to be made that multiple GP/SO management decisions ran contrary to industry standards, potentially contributing to ($) billions in cost overruns, including

- A failure to either include or implement multiple EPC contract……(Page 7)

- For the first 4-years of the project, GP/SO used only…..(Page 23)

- In 2017, it appears GP/SO did not validate critical underlying EPC…..(Pages 9- 10)

Analyzing 12-Years Of GP & SO Testimony… (Pages 20 & 23)

Please join us for our next Client Call at 12pm EST on Monday 10/26, to review our Vogtle Project Monitor. Please reach out to us for access details.

![]()

Table Of Contents:

- Key Takeaways – Page 2

- Who Owns $2.1B In Cost Overruns? – Page 3

- Georgia Public Service Commission 2018 Order – Page 4

- Cost Prudency Definition & Process – Page 5

- Decisions That Could Haunt GP/SO

- LSTK Contract Mismanagement – Page 7

- Bankruptcy – Parent Company Guarantee Settlement – Page 8

- Estimate to Complete – Page 9

- Transition from EPC LSTK to T&M – Page 10

- QRA – Cost – Page 11

- QRA – Schedule – Page 12

- GP Testimony & W|EPC Analysis (2009 to 2017

- EPC Contract Overview – Page 14

- October 2009 – Page 15

- October 2010 – Page 16

- April 2011 – Page 17

- November 2012 – Page 18

- June 2013 – Page 19

- October 2014 – Page 20

- October 2015 – Page 21

- December 2015 – Settlement of LD’s – Page 22

- December 2015 – Revised EPC Contract – Page 23

- October 2016 – Page 25

- April 2017 – Page 26

For access information, please email us at [email protected], or our institutional sales at [email protected]

Read More

Webber Research: Renewables Weekly

Webber Research: Renewables Weekly 10.20.20

Highlights:

• CEC Releases Clean Transportation Plan (page 1)

• New York Set 70% Renewable Energy Mandate By 2030 (page 1)

• ENPH Partners With Natura Living In Thailand (page 1)

• ENS Partners With alpha-Encorp (page 2)

• Bifacial Tariff Exemptions Blocked (page 2)

• JKS Signs Module Supply Agreement (page 2)

• CSIQ Adding Storage To GS Solar Farm (page 2)

• Enel Begins Construction Of Azure Sky Solar Project (page 2)

• Siemens Sub Acquires AMS (page 2)

• Proterra Raises $200MM (page 2)

• GE Wins 327MW Wind Order In India (page 2)

• SGRE Edges Out Vestas In Q2 (page 3)

• NOVA Expands Solar + Storage Offering (page 3)

• Arrival Raises $118MM From BlackRock Investment (page 3)

• PNM Plans To Replace Coal Plant With 1GW Solar + Storage (page 3)

• US Net Electricity Generation (pages 4-5)

• Solar PV Pricing (page 5)

• LCOE Benchmarks & Timeseries (page 6)

• Global Wind Turbine Market Share (Page 7)

• Global Solar PV Inverter Market Share (page 7)

• US Wind & Solar Projects Announced Or In Early Development (page 8)

CEC Releases Clean Transportation Plan: Last week, the California Energy Commission (CEC) released its clean transportation plan with ~$384MM of investments scheduled over the next 3 years for electric vehicle (EV) and zero-emission vehicle (ZEV) infrastructure. The spending includes ~$133MM for light-duty EV charging systems, ~$130MM for medium- and heavy-duty ZEV infrastructure, and ~$70MM for hydrogen refueling infrastructure. California currently has ~26MM automobiles and ~6MM trucks registered in the state – ~726k of which are ZEVs (vs its goal of 1.5MM by 2025 and 3MM by 2030). It also currently has 57k Level 2 chargers and 4.9k DC fast chargers vs its 2025 goal of 240k Level 2 and 10k fast chargers.

New York Set 70% Renewable Energy Mandate By 2030: On 10/15 New York’s Public Service Commission (PSC) announced it would formally adopt a 70% renewable energy initiative by 2030 as part of its Clean Energy Standard. The announcement includes a directive for NYSERDA to enter into annual contracts for 4,500MWh for upstate renewables and 700-1,000MW of offshore wind.

ENPH Partners With Natura Living In Thailand: On 10/12 ENPH announced it partnered with Natura Living to develop commercial solar projects in Thailand for PepsiCo (PEP). Natura installed a 60kW solar array on PEP’s snack division building using ENPH’s IQ 7+ microinverters and is currently installing another 60kW array on PEP’s agronomy division building (expected completion in Q420).

For access information, email us at [email protected], or go to webberresearch.com/downloads

Read More

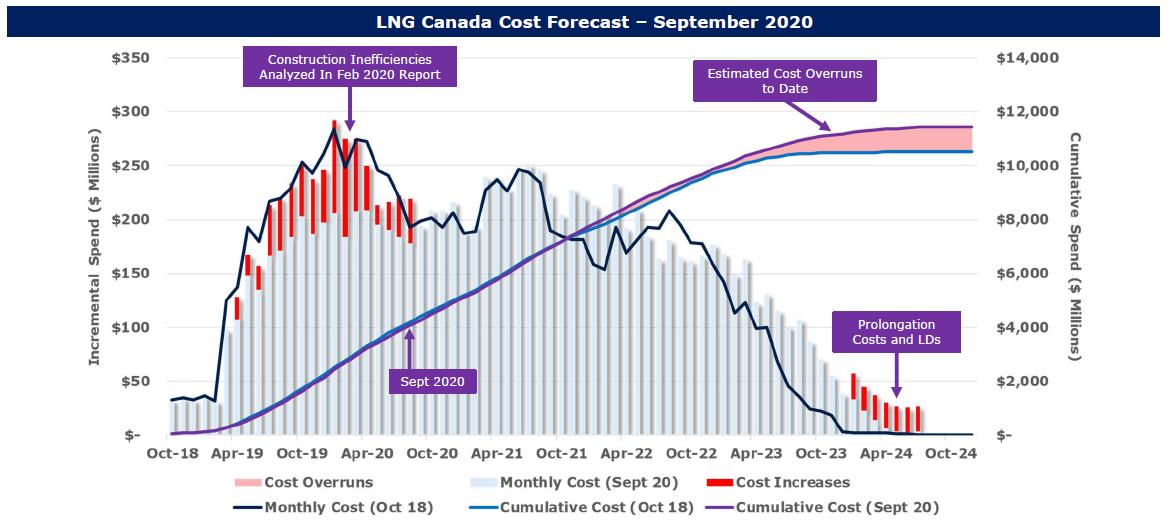

Webber Research: LNG Canada Q420 Update Call – Wednesday 10/21 at 12PM (EST)

Please join us for the latest Webber Research Client Call on Wednesday, 10/21 at 12PM, when we’ll discuss our latest thoughts on LNG Canada.

For access information, please contact us at [email protected], or our Institutional Sales Desk at [email protected]

W|EPC: LNG Canada – Updated Satellite Image Analysis & Construction Progress – Q420 Project MonitorRead More

Tradewinds 30-Year Anniversary: Meet The 30 People Who Will Shape Shipping’s Future – Michael Webber & Webber Research

https://www.tradewindsnews.com/twplus/meet-30-people-who-will-shape-shippings-future/2-1-879760

Read More

W|EPC: LNG Canada – Updated Satellite Image Analysis & Construction Progress – Q420 Project Monitor

Shell ∙ Fluor ∙ Mitsubishi ∙ PetroChina ∙ PETRONAS ∙ KOGAS

Table Of Contents:

- LNG Canada Q4 Monitor: Key Takeaways…………………………..….…Page 2

- LNG Canada Cost & Schedule Updates

- Updated Estimates…………………………..……………….….……..Page 4

- Project Milestones………………………………………………………Page 5

- Progress Analysis…………………………………………….….….….Page 6

- Analyzing Fluor’s 27.5% Reported Progress…….…………….……Page 7

- Project Staffing……………………………………………..……….….Page 8

- Satellite/Aerial Image Analysis

- July 2020 Overview………………….…………………….….………Page 10

- Sep 2020 Site Analysis……………………………………….………Page 11

- Jul vs. Sep 2020 – LNG Storage Tank…………………………..….Page 12

- Module Yard Analysis………………………………………………….Page 13

Key Takeaways:

- Delays At LNG Canada Continue to Build (Pages 4 – 7, 10 – 13)

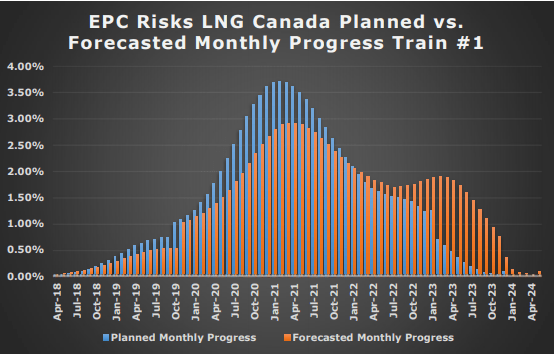

- Fluor reported ~27.5% Engineering, Procurement, Fabrication, & Construction (EPFC) progress in September, vs our current estimate of…

- We believe Fluor’s 27.5% guidance implies module fabrication progress of ~45%, which is ~9x…

- Fluor also referenced COVID-related project delays (without getting specific)

- Our Current Delay Estimate:…..

- Estimated Probability Of Maintaining Schedule:…..

- Mind The Gap: There are several potential explanations for such a degree of progress variance…

- Examining Fluor’s Goal of 2,500 On-Site Workers By Dec-20 (Pages 4, 8, 10 – 13)

- Aerial images suggest meaningful concrete, structural steel, and significant construction activities have yet to start (beyond piling)…

- Pre-COVID, Fluor’s reported onsite labor was higher than the project’s publicly reported staffing levels, leading to cost overruns (Pages, 4, 8)

- Limited construction work fronts could constrain Flour’s ability to…

- Kicking The Can Down The Road… LNG Canada Starting to Resemble Another Fluor/JGC Project… (Pages 4, 8)

- In 3Q13, CPChem awarded Fluor & JGC a ~$6B EPC contract for an Ethylene Cracker in Texas. ~39-months later, Fluor/JGC announced the project would be over budget. The project was finished in mid-2018 (a year behind its baseline plan).

- ~23-months after FID, we believe the LNG Canada (JFJV) schedule is slipping and costs are…

W|EPC: LNG Canada – Updated Satellite Image Analysis & Construction Progress – Q420 Project Monitor

For access information, please email us at [email protected], or our institutional sales at [email protected]

Read More

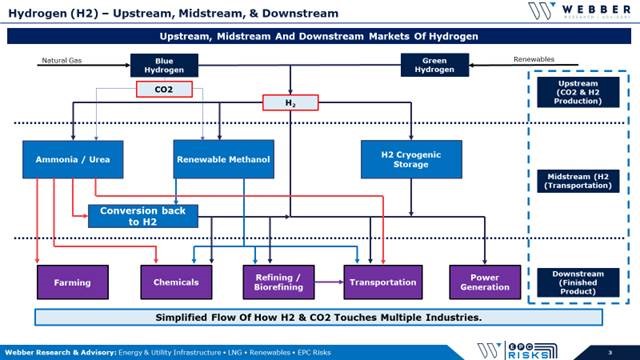

Hydrogen (H2) – The Production Process Roadmap – Upstream, Midstream, & Downstream – Q420

Hydrogen ∙ Ammonia ∙ Methanol

Table Of Contents:

- Key Takeaways And Flow Of H2 & CO2………………………………………Page 2

- Hydrogen’s Upstream

- Electrolysis Technologies & Market Leaders…………………….…..…Page 6

- Blue Hydrogen CO2 Issue………………………………………….…….Page 7

- Hydrogen Is Getting Cheaper………………………………………….…Page 8

- Carbon Capture Systems & CO2’s Critical Role…………..………..…Page 9

- Hydrogen’s Midstream – Transportation

- Ammonia Transportation – Green Hydrogen………………..….…….Page 12

- Methanol Transportation – Blue & Green Hydrogen……………..….Page 14

- Cryogenic Hydrogen Energy Loss Concern…………………….……Page 16

- Closer Look – Ammonia vs Methanol

- Hydrogen Comparison…………………………………………………Page 18

- Example Product Comparison…………………………………………Page 19

- Converting Back To H2…………………………………………………Page 20

- Ammonia & Methanol Co-Production Facilities………..….………..Page 21

- Marine and Fuel Cell Comps

- Industry Impact – H2 Transportation…………………………………Page 23

- IMO Driving LNG, Ammonia Or Methanol Fuel For Ships….……..Page 24

- Carbon Neutral Marine Fuels – IMO 2050………………………….Page 25

- Ammonia & Methanol Co-Production Facilities…………………….Page 26

- Technology Leaders and Applications

- H2 – Industry Technology Leaders………………………………….Page 28

- Applying Technology In The EPC Process…………….………..…Page 29

- Technology Packaging & Trends…………………………….….….Page 30

Key Takeaways:

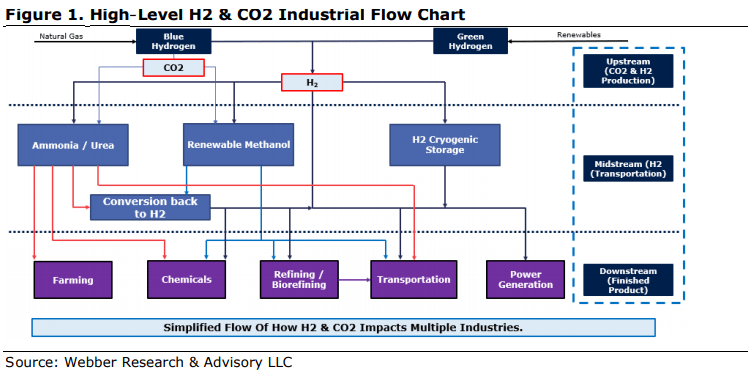

Upstream Sources Of Hydrogen – Blue & Green (Pages 4 – 9)

>95% of Hydrogen (H2) is produced using Steam Methane Reformer (SMR) technology that produces 7 units of CO2/unit of H2 (on average)

SMR w/ a carbon capture system (Blue H2) is the preferred option to environmentally manage excess CO2. (page 7)

Green H2 provides minimal CO2 but current technology limits Green H2’s cost competitiveness. (Page 6)

H2’s Sprint To Market Share… Current Leaders (Pages 17 – 21, 27 – 30)

We analyzed 13 Technology Companies spanning 12 Process industries, including ThyssenKrupp, Air Products, Air Liquide, & KBR/Johnson Matthey…the clear technology leaders include…

Frozen Industries – Marine, Automotive, & H2 Transport (Pages 22 – 26)

Outside factors (i.e. carbon neutral fuels, fuel cells, regulations, safety, & other downstream applications) will play a large role in selecting the midstream transportation choice for H2.

International Maritime Organization’s (IMO) mandates for reduced emissions has many ship builders looking at LNG, Ammonia, and/or Methanol; without a clear long-term winner (yet), many shipbuilders are frozen.

Fuel pumps (gas stations) must receive H2 from high-pressure storage vehicles, pipelines, or by converting Methanol or Ammonia to H2 at the fuel pump, with a number of implications.…(page 20)

Midstream For Hydrogen – H2 Transportation Options (Pages 10 – 16)

Ammonia, Methanol, and Cryogenic H2 are used to transport H2 long-distances.

Ammonia is the clear favorite to…

Methanol is the best option for…

Cryogenic H2 technology/costs…

For access information, please email us at [email protected], or our institutional sales at [email protected]

Read More

Renewable Energy: Expanding Our Hydrogen & Solar Coverage

Initiating Coverage Of PLUG, BLDP, & SEDG

Plug Power (PLUG)

Company Overview – Page 5

Plug Symposium (Raw Notes) – Page 10

Investment Rationale / Key Points – Page 12

Primary Risks – Page 14

Valuation – Page 15

Ballard Power Systems (BLDP)

Company Overview – Page 22

Analyst Day (Raw Notes) – Page 28

Investment Rationale / Key Points – Page 35

Primary Risks – Page 36

Valuation – Page 37

SolarEdge Technologies (SEDG)

Company Overview – Page 45

Investment Rationale / Key Points – Page 48

Primary Risks – Page 49

Valuation – Page 50

Industry Overviews

Hydrogen & Fuel Cells – Page 55

Solar / Inverters – Page 67

Expanding Our Hydrogen & Inverter Coverage. We are initiating coverage of PLUG (Outperform, PT: $19), BLDP (Outperform, PT: $26), and SEDG (Market Perform, PT: $200). Since launching our first wave of coverage in April (REGI – OP, ENPH – MP, TPIC – MP, and ENS – MP) renewables have continued to aggressively take both mind-share and market-share – positioning the sector for unprecedented investment as governments, counterparties, and end-users move toward carbon neutrality over the next 15-40 years. Benchmark renewable levelized cost of energy (LCOE) figures have declined nearly 75% over the past-10 years, increasing the viability of alternative energy sources. We believe the extension of that process toward low- and zero-carbon hydrogen could create a generational growth engine across Energy, Industrials, and Technology over the next several decades.

The Push For Hydrogen: Major markets worldwide continue to adopt integrated hydrogen strategies and roadmaps, with Europe and China at the forefront. The EU is expected to invest €183-€490B by 2050 to effectively develop a continental hydrogen economy, with green hydrogen (i.e. hydrogen created using renewable sources) at its center. China recently announced its National Hydrogen Fuel Cell Strategy and pledged to reach carbon neutrality by 2060 despite currently deriving two-thirds of its power from coal. We think the increasingly widespread support for carbon-reducing policy creates a deliberate and sturdy foundation for renewables, and particularly hydrogen.

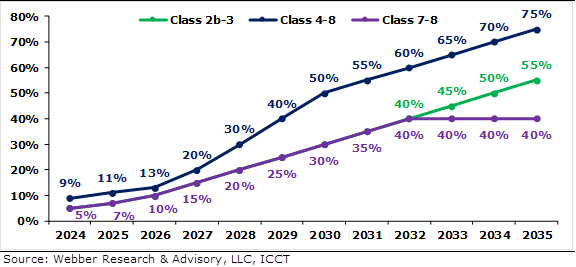

Figure 58. California Advanced Clean Truck Regulations

Figure 50. Hydrogen Production Costs From Renewables & Fossil Fuels

For access information, please email us at [email protected]

Read More LNG Canada construction delay creates cost uncertainty, clouds world supply

Read More Webber Research: Technical & Commercial Project Consulting

Webber Research: Technical & Commercial Project Consulting Overview

We’re very pleased to share our most recent Webber Research Technical & Commercial Project Consulting Overview – detailing our expertise across a wide variety capabilities, services and experience. If you’re a project stakeholder, developer, creditor, or operator, we’re here to add value and minimize risk for your process.

Webber Research: Technical & Commercial Project Consulting Overview

Our Focus: LNG, Biofuels, Renewables, Petrochemicals, and broader Energy Infrastructure

Key Experience, Capabilities & Services:

• Proprietary Project Database: Includes schedules, satellite & drone images, & benchmarks

• Lenders/Stakeholder’s Independent Engineer: $50B+ of global project’s executed

• Commercial & Contracts Negotiations: Negotiated ~$30B in EPC proposals/contracts

• Government/Regulatory Liaison: FERC, U.S. Army Corps of Engineers, etc.

• Project Due Diligence: ~$1.5B investment that grew to ~$7B in ~8 years

• Validate Schedule/Progress Reporting: Helping independent stakeholders can avoid surprises

• Litigation Consulting/Claims: Supporting more than $1B in litigation, depositions, and expert witness

Unmatched Process. Industry Changing Results.

Read More Chinese container factories are now sold out until February – More evidence of US container import strength

https://www.freightwaves.com/news/chinese-container-factories-sold-out-until-february

Read More ESG – Moving Into A More Transparent Future

https://www.seatrade-maritime.com/opinions-analysis/esg-moving-more-transparent-future

Read More

Webber Research: Renewable Biofuels – Refinery Conversions, Crack Spreads, & Risks Q420

Renewable Biofuels – Refinery Conversions, Crack Spreads, & Risks Q420

- Key Takeaways (page 2)

- Biofuels – Costs, Risks, & Incentives (page 3)

- Renewable Fuels vs. Traditional Refining Economics (page 4)

- Crack Spread Analysis – Ratios Matter (page 5)

- The California Renewable Fuel Rush (page 6

- Biofuels & Soybean Oil Supply/Demand (page 7

- Biofuels Project Tracker (page 8)

- Hydrogen’s Increased Demand in Biorefining (page 9)

- HVO vs FAME Biofuel (page 10)

- PSX’s Rodeo Refinery Conversion (page 11)

- Rodeo Refinery Conversion Overview (page 12)

- PSX Project Comp – WA vs. CA (page 13)

- EPC Dynamics (page 14)

- EPC Contractor Rankings (page 15)

Key Takeaways:

- Renewable Fuel Production… Just in Time or Too Late? (Pages 4 – 8)

- California & Oregon have mandated Carbon Intensity (CI) reductions in transportation fuels, which could increase demand by ~350%, from ~400MM gallons/year to 1,400MM by 2025. Ten other states are evaluating similar LCFS programs, which could potentially push U.S. demand toward 2,400MM gallons/year, up ~600%…

- Refinery Conversions: FAME vs. HVO (Page 10)

- Emerging trend in Biofuels: a transition from Fatty Acid Methyl Ester (FAME) to Hydrotreated Vegetable Oil (HVO), which provides biofuels a longer storage life & can be used in colder climates.

- FAME & HVO biofuels are produced using a refinery’s hydrotreater & isomerization, or a hydrocracking unit with a steady supply of hydrogen. HVO economics are dependent on hydrogen prices & feedstock ratios.

- Hydrogen’s Increased Demand in Biorefining (Page 10)

- As of early 2020, traditional oil refining consumed ~1/3 of the global Hydrogen demand.

- FAME biorefining requires similar Hydrogen consumption relative to traditional refining, but HVO biorefining uses significantly more Hydrogen depending on the process units…

- Speed To Market Matters: Owners, Operators, & Contractors (Pages 12, 13, 15)

- ~10 years ago, companies were chasing another speed to market trend, NGL production and fractionation. Flexible and decisive companies (e.g. EPD, ET, etc.) quickly capitalized on this opportunity and captured market share.

- Large Energy companies (e.g. Exxon, Shell, etc.) are not typically structured to move quickly refining industry (VLO, PSX, MPC) and take on the speed to market risk..

W|EPC: Renewable Biofuel Analysis Refinery Conversions, Crack Spreads, & Risks Q420

For access information, please email us at [email protected] or visit our website at webberresearch.com

Read More

Webber Research: Hydrogen Tracker

Webber Research: Hydrogen Tracker 09/09/2020

Recent News (page 1)

M&A Tracker (page 3)

Valuation Summaries (page 3)

Hydrogen Production Costs (page 4)

Industry/Background (page 6)

LH2 Carrier Progress (page 7)

• GM Forms Strategic Alliance With Nikola: On 9/8, GM announced it took an 11% ownership stake in Nikola (NKLA) worth ~$2B as well as the right to elect one director to NKLA’s Board, in exchange for in-kind services. GM will engineer and manufacture the Nikola Badger (both the BCEV and FCEV models), and will be the exclusive supplier of fuel cells globally (except in Europe) for NKLA’s Class 7/8 trucks (heavy-duty trucks, including the Nikola Badger, Nikola Tre, Nikola One, Nikola Two and the NZT), utilizing its Ultium battery system and Hydrotec fuel cell technology. NKLA said it expects to save more than $4B in battery and powertrain costs over 10 years and $1B+ in engineering and validation costs, while GM expects to receive in excess of $4B of benefits from the equity value of NKLA shares, contract manufacturing of the Badger, supply contracts for batteries and fuel cells, and EV credits retained over the life of the contract. GM will be subject to a staged lock-up period (beginning in 1 year and ends in June 2025). The Badger will make its public debut 12/3-12/5 at Nikola World 2020

• Ballard Markets First Fuel Cell Designed For Marine Vessel Propulsion

• Siemens Announces Green Hydrogen Systems As Electrolysis Partner

• California Regulators Funds 36 More Hydrogen Stations

• Australia’s First Green Hydrogen Plant

• Germany Eyes Hydrogen Project In Democratic Republic Of Congo

• Freudenberg Sealing Technologies To Develop Special Fuel Cell System For HeavyDuty Trucks

• SunHydrogen Expands Partnership With University Of Iowa

• Wystrach Reveals Its Mobile Hydrogen Refueling Station

M&A Tracker

• 6/23/20 PLUG Acquires United Hydrogen & Giner ELX:

• Total consideration of ~$123MM (~$65MM for United Hydrogen and ~$58MM for Giner ELX).

• United Hydrogen is a merchant hydrogen producer in North America with production capacity of 6.4t/d with plans to expand to 10t/d.

• PLUG previously announced it held a convertible bond in United Hydrogen which could represent over 30% equity ownership on a converted basis.

• Giner ELX provides PEM hydrogen generators, grid-level renewable energy storage solutions, and onsite generation systems for fuel cell vehicle refueling stations.

• PLUG increased its 2024 financial targets to $1.2B in revenue (from $1.0B), $210MM in operating income (from $170MM), and $250MM in adjusted EBITDA (from $200MM).

For access information, email us at [email protected], or go to webberresearch.com/downloads

Read More

W|EPC: Renewable Methanol & Hydrogen – Analyzing Methanex’s (MEOH) Geismar Facilities

Renewable Methanol & Hydrogen – Analyzing Methanex’s (MEOH) Geismar Facilities – September 2020

- Methanex & Renewable Methanol – Key Takeaways (page 2)

- Renewable Methanol (page 3)

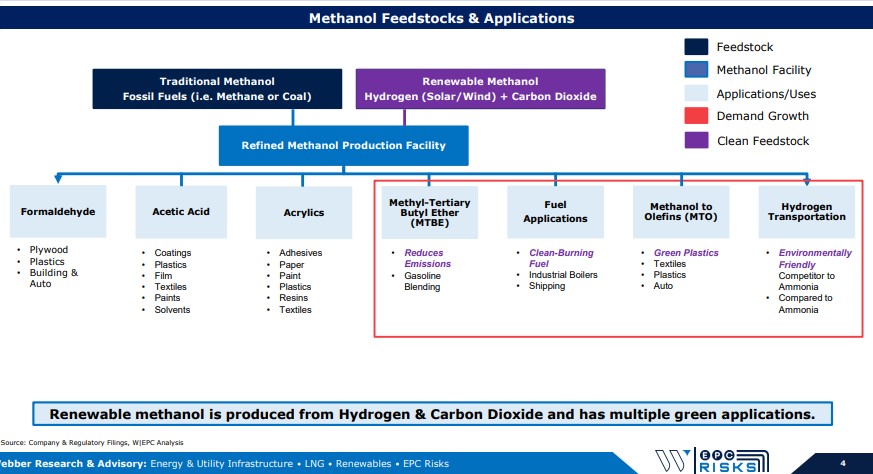

- Methanol Feedstock & Applications (page 4)

- Hydrogen is Getting Cheaper (page 5)

- Renewable Methanol Facilities (page 6)

- Geismar Methanol Facilities (page 7)

- Methanex Overview (page 8)

- History – Geismar Units 1 & 2 (page 9)

- Geismar Unit 3 Comps (page 10)

- GU3 Cost Overview (page 11)

- Schedule – Key Milestones & Impact (page 12)

- Monthly Progress Curves (page 13)

- EPC Dynamics – So Long KBR, Next Up?(page 14)

- Disclosures (page 15)

Lower-Cost Hydrogen Will Produce Cost Competitive Renewable Methanol: Pipe Dream or Reality? Global methanol demand sits near ~75 MTPA; with demand expected to ramp amid new EU and U.S. environmental mandates. Renewable Methanol (RM) is produced using Hydrogen (H2) from solar/wind and carbon dioxide (CO2) as compared to traditional methanol produced from fossil fuels (i.e. coal & natural gas). (Page 4)

Cost-competitive RM would open the door to green plastics and support various marine, fuel, & vehicle clean energy mandates but, costs are not competitive based on current technology. (Pages 4 – 5) Limited project economics hasn’t stopped ~10 commercial scale renewable methanol facilities in various stages of development around the world. As these projects develop, lower costs and improved technology would be a game changer for the methanol industry while providing H2 more downstream applications. (Page 6)

Tracking the 800 lbs. Methanol Gorilla…Methanex (MEOH). (Pages 8 – 9)

Geismar Unit 3 – Positioning vs. Competition. (Pages 10 – 13)

For access information, please email us at [email protected] or visit us at webberresearch.com

Webber Research Broadens Hydrogen, Renewables, & Biofuel Technical Expertise Through Expansion of W|EPC Strategic Partnership

Read More

W|EPC: Golden Pass LNG (XOM, QP) – Project Update & On-Site Satellite Image Analysis – Q320

Golden Pass LNG: Our Delay & Contingency Fund Estimates Continue to Ramp

Key Takeaways:

• Chiyoda’s Engineering Delays Continue. We believe engineering delays have eroded a significant portion of the EPC risk, contingency, and profit, with the likelihood of ramping balance sheet exposure. (Pages 4 & 11)

• Our updated project timeline (delay) and contingency fund estimates are now material, sitting at….(continued)

• Our estimates point to Golden Pass project progress sitting closer to ~10% vs Chyioda’s report figure of 16% (Q2) based on both our satellite image review and….(continued)

• Sabine Pass Comparison. 18-Months after FID Sabine Pass LNG Trains 1 & 2 were 57.1% complete, vs our estimated range for Golden Pass LNG (~10-16%). (Page 8)

Table Of Contents

- Golden Pass Q320 Update – Key Takeaways (page 2)

- Revised Cost & Schedule Forecasts (page 3)

- Cost Forecast (page 4)

- Project Milestones (page 5)

- Progress Analysis (page 6)

- Analysis – Chiyoda’s 16% Reported Progress (page 7)

- Putting It All Together – W|EPC Updated Contingency fund and project delay estimates

- 18-Months After FID, Sabine Pass vs. Golden Pass LNG (page 8)

- Joint Venture Analysis (page 9)

- Change Order Analysis vs. JV Structure (page 10)

- Possible Impacts to Chiyoda (page 11)

- Satellite Image Analysis (page 12)

- Disclosures (page 17)

Golden Pass LNG Satellite Image Overview (page 13)

For access information please email us at [email protected]

W|EPC: Golden Pass LNG – Delay & Contingency Fund Estimates Continue To Ramp – Updated Project & Satellite Image ReviewRead More

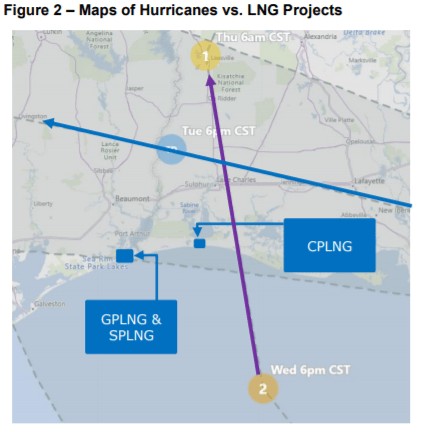

W|EPC: Assessing Force Majeure Impact on Calcasieu (Venture Global), Golden Pass (Exxon, QP) & Sabine (Cheniere)

Webber Research – Energy EPC

Marco & Laura Impact Could Last 7 to 14 Days…Depending on Damage & Craft Labor Retention

EPC contractors receive schedule relief for Force Majeure (FM) events (i.e. named storms such as Marco & Laura) in industry standard EPC contracts, which typically provides EPC contractors schedule relief but not cost relief.

EPC contractor FM claims on Calcasieu Pass, Golden Pass, and Sabine Pass LNG likely started yesterday August 24th, 2020 (due to mandatory evacuations & closures).

Something to watch…construction workers tend to scatter and chase higher paying (wages & per-diem) jobs post hurricanes/natural disasters, which creates headaches for on-going/planned projects and complicates FM claims.

Based on current Marco & Laura forecasts and expected rain/storm surge, we are forecasting a 7 to 14-day construction schedule delay on Calcasieu Pass LNG (CPLNG), Golden Pass LNG, & Sabine Pass LNG Train #6 (SPLNG6).

Impact & Timeline Implications

Often, impacts due to hurricanes occur well beyond the actual storm itself due to lost productivity and challenges restarting/staffing the project.

Flooding – enough drainage pumps installed and site drainage working sufficient to mitigate additional rain fall.

Storm Surge – levees/walls high enough to protect rising levels and all equipment moved to the highest elevation on the site (if practical).

Wind – cranes must be placed horizontally and structures secured to reduce/prevent damage.

Temporary Construction Facilities – if levees and/or drainage are not in place at temporary construction facilities, equipment and material stored in laydown yards/facilities could be damaged by water and cause unplanned long-term issues.

EPC contractors have a reputation for trying to use FM impacts to absorb existing self-inflicted schedule delays. Based on the current/expected forecast, we believe the following FM timeline is realistic.

Prep time for storms – 1 to 3 days

Marco & Laura storm duration – 2 to 4 days

Restart & productivity losses – 4 to 7 days

Our specific estimates and thoughts on individual projects in the pages that follow:

For subscription information, email us at [email protected]. For more information on this note, please visit our online store at webberresearch.com/downloads

Read More HL Acquisitions Corp and Fusion Fuel Green Ltd Amend Business Combination Agreement and Sign Commitments for $25M Capital Raise

Read More

W|EPC: Gorgon LNG – Operational Breakdown Could Have Contributed To Kettle Cracks – Mid-October A More Likely Restart Timeline

W|EPC: Gorgon LNG – Operational Breakdown Could Have Contributed To Kettle Cracks

Mid-October May Be A More Likely Restart Timeline

Key Takeaways:

Pump The Brakes: While potential fabrication errors have been the primary narrative around the Propane Kettle cracks that shut down Gorgon LNG, it’s feasible that operational issues (and one in particular) may have contributed or even partially caused the cracks on Train-2’s kettles, which could have significant and more complex implications.

- The propane kettle cracks were noticed ~3-years after the kettles were placed in-service (likely beyond any warranty period), potentially shifting costs to Chevron.

- According to our in-house engineers, a breakdown in the propane vapor transfer step could subject the propane kettles to temperatures significantly below the minimum design metal temperature; creating stress on the metal and an optimum environment to cause cracks.

- If the root cause involved an operational issue, it would require not just replacement or repairs, but more robust inspections, testing, and training, which would add to the out-of-service timeline (below).

- If a breakdown in the propane vapor transfer step did contribute to the cracks, it would have likely needed to be repeated routinely to cause the visible cracks on Train-2, increasing the likelihood that such an error would have been repeated on Trains 1 and 3 as well, given the likelihood of crew rotation.

Timeline Implications

According to recent press reports, Chevron has suggested an early September restart for Train 2 and provided train 1 & 3 inspection time-frames.

- Train 2 – Currently Down since July, Online Sep 20

- Train 1 – Shutdown Early Oct 20, Online Nov 20 to Jan 21

- Train 3 – Shutdown Jan 21, Online Mar 21 to Apr 21

- We think mid-October for Train 2 may be more realistic. While the repairs themselves may fit within a mid-September target, we believe a thorough assessment of the route problems, inspections, training, etc., likely push out the downtime. We don’t know yet what approvals and 3rd party reviews will be necessary to confirm the repairs were made in a satisfactory way, but this could impact the timelines given as well. Continued…

For access information please email us at [email protected]

Read More

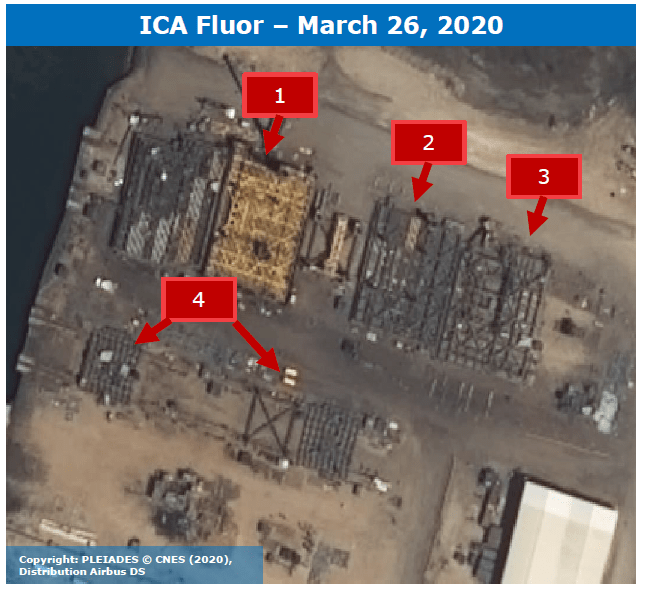

W|EPC: Venture Global LNG – August 2020 Update

W|EPC: Venture Global & Calcasieu Pass LNG – Satellite Image Review (ICA & Fluor) & More Engineering Changes.

Key Points:

- Calcasieu Pass Revises Key Engineering Documents (Again). Over the past two weeks Calcasieu Pass (CPLNG) submitted engineering updates to FERC, most of which are marked as confidential. While the substance of the updates and revisions are unknown, the types of documents that were filed indicate possible changes to structural steel design & calculations, equipment flow rates, and the project’s mechanical equipment list. (Page 4)

-

Q2 Progress: Pre-Treatment Unit Module Fabrication – ICA Fluor & the Tampico, Mexico fabrication yard. As previously noted, we believe ICA Fluor is fabricating the CPLNG Pre-Treatment Unit (PTU) Modules in their Tampico, Mexico fab yard. Satellite images show

-

Pre-FID Feedstock Specs Or Assumptions May Have Changed…

Calcasieu Pass LNG August Update – Key Takeaways.- Page 2

More Engineering Adjustments – Page 4

Changes To Feedstock Assumptions?- Page 4

Satellite Image Analysis – ICA Fluor (Tampico, Mexico) – Page 5

Pre-Treatment Unit Module Overview – Page 6

March vs. July 2020 – ICA Fluor Satellite Image Comparison – Page 7

Closer Look – March 2020 – Page 8

Closer Look – July 2020 – Page 9

Disclosures – Page 10

Previous ICA Fluor Satellite Image

W|EPC: Venture Global LNG: August 2020 Update

For access information, email us at [email protected], or visit our online store at webberresearch.com/downloads

Read More

W|EPC: LNG Canada Q320 Monitor – Labor Dynamics & Baseline Satellite Image Review

LNG Canada Q320 Monitor – Labor Dynamics & Baseline Satellite Image Review

Shell • Petrochina • Mitsubishi • Kogas • Petronas

1) Union Craft Avg. Wage Rate Escalators & Impact On JGC/Fluor, and broader project cost…

What’s Happened/Changed: Part of our current focus is on LNG Canada’s wage rate escalation and union labor agreements post-2023.

Why Does That Matter: EPC lump sum proposals generally include labor escalation between 1-3% per annum (rates vary based on geography/availability). Labor agreements supporting LNG Canada and other B.C. projects expire in 2023 and have a relatively advantageous average labor escalation rate of…..continued.

For context, union labor strikes, renegotiated agreements, and significant wage rate escalation supported Gorgon LNG coming in $20B+ over budget.

What’s The Impact:…..continued (Page 3)

2) Taking A Look At JFJV’s Longer-Term Labor Inflation Risk (Page 5)

3) JFJV’s Construction Activity – What does it tell us about the project timeline? (Page 8)

4) Satellite Image Analysis Baseline – Benchmarks for Remainder of the Project…. (Pages 9-17)

W|EPC: LNG Canada Q320 Monitor – Labor Dynamics & Baseline Satellite Image Review

For access information please email us at [email protected]

Read More

W|EPC: Gorgon LNG’s Propane Kettle Cracks – Early Read

Overview:

On July 23, 2020, Reuters reported Australia’s Department of Mines, Industry Regulation & Safety (DMIRS) said “it plans to inspect Chevron’s Gorgon LNG plant as soon as possible following calls by a trade union to shut the plant.”

1. During routine maintenance, Chevron Australia discovered issues with the propane kettles on Train #2.

2. “The Australian Manufacturing Workers’ Union (AMWU) has called for Chevron to shut down the Gorgon plant for immediate safety inspections by a gov. regulator and for a report to be made public.”

3. Specifically, cracks up to 1 meter long and 30 millimeters deep were discovered by the non-destructive testing team (per AMWU). On July 28, 2020, a Chevron company spokesman said, “Chevron expected to restart Train #2 of its Gorgon LNG plant in early September after completing repairs.” Chevron said during routine maintenance that began on May 23rd and was scheduled to be completed by July 11, 2020, weld quality issues were discovered on 8 propane heat exchangers. Gorgon LNG Trains 1 & 3 are producing. On 07/29/20, inspectors from DMIRS were due on site to inspect the cracks after AMWUraised issues about the conditions of the South Korean-made kettles.

Key Takeaways:

• Inspectors from Western Australia’s “safety watchdog” were scheduled to inspect propane kettle cracks on Chevron’s Gorgon LNG Train-2 on 7/29

• Labor unions continue pushing back, requesting a full shut down of all three LNG trains for inspection.

• Publicly available technical details are limited, even for the folks who built Gorgon LNG (who we spoke with); however, we believe the 3-month estimated down time for repairs is….continued

• Primary rationale for a Train-1 and Train-3 inspection shut down would be…continued

W|EPC Thoughts & Observations

The publicly available technical details are limited, even for our contacts involved in building Gorgon LNG. However, we are watching the following:…continued

Concluding Thoughts…

Key Questions…

For access information please email us at [email protected]

Read More

Webber Research: Hydrogen Tracker Highlights:

- Recent Highlights (page 1)

- LH2 Carrier Progress (page 3)

- M&A Tracker (page 4)

- Valuation Summaries (page 5)

- Hydrogen Production Costs From Fossil Fuels (page 6)

- Hydrogen Production Costs From Renewables (page 7)

- Hydrogen Projects & Electrolyzer Tech (page 8)

- Fuel Cell Technology Comparisons (page 9)

Recent Highlights

NKLA Breaks Ground On Coolidge Facility: On 7/23 NKLA announced it began construction on its 1MM sqft……

NEE Eases Into Hydrogen: On 7/24 NEE proposed a $65MM pilot green hydrogen plant with a 20MW electrolyzer in Florida….

MSFT To Replace Diesel Backup Power With Hydrogen: On 7/27 MSFT announced it successfully powered a row of data center servers for 48 consecutive hours with a 150kw hydrogen fuel cell system….

Linde To Build Refueling Station For World’s First Hydrogen Passenger Train: LIN will build and operate the station and is expected to begin construction in… BKR & Snam Complete Testing On Hybrid Hydrogen Turbine: On 7/20 BKR and Snam announced the successful testing of the hybrid hydrogen-powered NovaLT12 turbine

Read More

Petroleum Economist: Stars Have Aligned For The Hydrogen Economy

Read More

W|EPC: Venture Global & The Approach Nexus – Drone & Satellite Image Analysis, Engineering Changes Q320

W|EPC: Venture Global – Nexus Approaching Drone &Satellite Image Analysis, Engineering Changes Q320

For access information, visit our New Online Store, or email us at [email protected]

• Calcasieu Pass Update – Key Takeaways (slide 2)

• Calcasieu Pass LNG Module Overview (slide 3)

• Importance Of Notification Window (slide 4)

• Engineering Changes: Pre-Treatment Modules (slide 5)

• Engineering Changes: Liquefaction Modules (slide 7)

• Technical Analysis: Changes & Impact? (slide 9)

• Satellite Image Analysis – Baker Hughes Module Yard (slide 13)

• Drone Image Analysis – Site Prep Update (slide 18)

• Remaining Questions (slide 23)

• Scenario Analysis & Predictions – Rubber Starting To Meet The Road? (slide 25)

• Disclosures (slide 27)

Key Highlights:

• Venture Global: The Looming EPC Nexus…

• Drone Image Analysis:

• Calcasieu Pass Outlook

• Consequential Damages, Predictions & Conclusions

Copyright: PLEIADES © CNES (2020), Distribution Airbus DS & W|EPC Analysis

For access information, email us at [email protected]

Read More

Webber Research Hydrogen Tracker

Introducing the Webber Research Hydrogen Tracker

Yesterday we launched our Hydrogen Tracker – a weekly research product dedicated to the build out of Hydrogen production, technologies, and associated markets. For information about access to our Hydrogen Research, Renewables, or our Utility, Energy, & LNG Infrastructure Project coverage, please email us at [email protected]

Highlights:

• Recent News (page 1)

• LH2 Carrier Progress (page 3)

• M&A Tracker (page 4)

• Valuation Details (page 4)

• Hydrogen Production Costs (page 5)

• Demand Trends (Page 7)

• Electrolyzer Market Share & Technology Growth (page 8)

- Data & Updates:

- EU Hydrogen Strategy: On 7/8 the European Commission provided additional details on its broader energy transition including its hydrogen strategy…

- APD, ACWA Power, & NEOM Form JV For $7B Green Hydrogen Facility In Saudi Arabia: On 7/7 APD announced, in conjunction with equal JV partners, ACWA Power and NEOM, the signing of a $5B agreement for a global-scale green hydrogen-based ammonia production facility…

- Air Liquide & Port of Rotterdam Joint Initiative For Hydrogen Trucking: On 7/6 Air Liquide (AI-FR) and the Port of Rotterdam Authority announced a joint initiative to adopt and build the infrastructure for 1,000 hydrogen-powered zero-emission trucks by 2025…

- CARB Passes Zero-Emission Truck Regulations: On 6/25 the California Air Resources Board (CARB) passed the Advanced Clean Trucks (ACT) Regulation which accelerates the large-scale transition of zero-emission medium and heavy duty vehicles in California. Beginning in 2024, 9% of all on-road Class 4-8 trucks sales…

- NEL +NOK 150MM Purchase Order: On 6/30 NEL announced a +NOK 150MM purchase order for multiple H2Station units from…

- BLDP $7.7MM Purchase Order From JV: On 7/2 BLDP announced it received a $7.7MM purchase order of membrane electrode assemblies (MEAs) for use in…

- NKLA Starts Preorders: On 6/29 NKLA opened preorders for its Badger pickup truck, NZT off-highway vehicle (OHV), and WAV jet ski…

- FCEL Terminates Exclusivity Agreements With POSCO, Seeks +$200MM In Compensation: On 6/28 FCEL officially notified POSCO Energy and…

…continued

For access information, please email us at [email protected]

Read More

W|EPC: Dominion Energy (D) – Offshore Wind Project Monitor Q320

W|EPC: Dominion Energy (D) – Q320 Offshore Wind Project Monitor

- Dominion Energy (D) Q320 Capital Project Monitor: Key Takeaways (slide 2)

- Virginia Clean Energy Act – Why Should You Care? (slide 3)

- Energy Costs vs. Benefits (slide 4)

- Coastal Virginia Offshore Wind (CVOW) Project Overview (slide 5)

- Phase #1: A Closer Look At The Pilot Project (slide 7)

- Regulatory Approval Timeline

- EPC Contractor – Ørsted

- Cost & Schedule Analysis

- Phase #2: The $8B Main Course (slide 13)

- Overview & Status

- How big Are 12MW Offshore Turbines?

- Offshore Wind: Construction, Risk, & Insurances Overview (slide 16)

- Conclusions: Thank A Rate Payer (slide 20)

Key Highlights:

• Offshore Wind… An Awesome Opportunity for Dominion, Right?

• Phase #1 Demonstrator Costs Ballooned By ~73%…

• Phase #2 (2.6GW) Is The Real Prize – But Definitely Worth Keeping An Eye On Costs…

For access information please email us at [email protected]

Read More

Webber Research: Renewables Weekly

Renewable Energy Highlights:

For access information email us at [email protected]

- Wild Week For ENPH (page 1)

- PLUG Acquires United Hydrogen & Giner ELX (page 2)

- BLDP Follow-On Order From Wrightbus (page 2)

- JinkoSolar To Supply Bifacial Modules In Chile (page 2)

- RUN To Launch 2 Virtual Power Plants (page 2)

- FCEL Restarts Operations At Torrington, CT Facility (page 2)

- NOVA Closes Solar Backed Notes (page 2)

- NEL +$3MM Purchase Order (page 2)

- GE Nearly Doubling Headcount At LM Wind Facility (page 2)

- SGRE SG 14-222 DD Turbine Backlog Up To 4.3GW (page 2)

- MHI Vestas Supplier Begins Taiwanese Blade Facility Construction (page 3)

- Vestas Recent Order Summary (page 3)

- Denmark To Develop First Offshore Wind Energy Islands (page 3)

- Germany’s National Hydrogen Strategy (page 4)

- New Jersey Plans Offshore Wind Port (page 4)

- EPA Receives 52 New SREs For 2011-2018 (page 4)

- Australian Storage Capacity To More Than Double In 2020 (page 4)

- US Net Electricity Generation (pages 5-6)

- Solar PV Pricing (page 6)

- LCOE Benchmarks & Timeseries (page 7)

- Global Wind Turbine Market Share (Page 8)

- Solar PV Inverter Market Share (page 9)

- US Wind & Solar Projects Announced Or In Early Development (page 10)

Wild Week For ENPH: Last week ENPH traded down 26% on the back of a short report alleging various accounting violations and more serious fraudulent activity, before recovering most of the lost ground in the days that immediately followed (-4% on the week). From our perspective, the report highlights a number of red flags, however…..

For access information email us at [email protected]

Read More

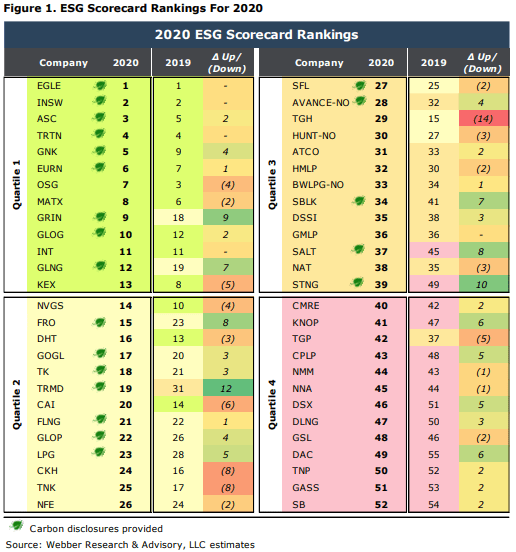

Webber Research ESG Scorecard: 2020

2020 ESG Scorecard – Updated Model, Same Idea. Before we delve into our updated rankings, framework, and company specific changes, we want to reiterate the idea that underpins this entire endeavor, which is that we believe there is no longer a place in the public shipping markets for companies that do not prioritize strong corporate governance and capital stewardship. We believe that risk premiums associated with poor governance and capital discipline should continue to widen, eventually pricing-out conflicted players and antiquated structures from public markets.

New Carbon Factor. Our 2020 ESG Scorecard includes a broadened methodology that incorporates the public disclosure of relevant of carbon data, which becomes the 9th factor within our proprietary multi-factor ESG model and increases the total number of subfactors to 20 (from 18). The carbon disclosure metrics we’ve chosen to initially include (AER & EEOI – see Page 15) are aimed at aligning our ESG framework with the Poseidon Principles, and intended to help facilitate the consistency and disclosure of carbon data to investors. We will also continue to display each company’s ESG Scorecard Quartile, as well as a Carbon Disclosure Indicator on the front page of our company-specific research notes – as we’ve done since we launched Webber Research in Q419.

Model Adjustments. We’ve given our new Carbon Factor a 20% weighting within our model, positioning it among the most dominant variables within our framework, while re-weighting other aspects of our model in order to accommodate the addition. Our revised factor weightings and methodology can be found on Pages 10-15. We also narrowed our 2020 ESG Scorecard universe to 52 companies from 56 (Page 5).

Carbon Disclosure: Who’s Participating? We’ve included a summary of our work around carbon disclosures on Pages 2-3. In total, 42% of the companies in our scorecard (22/52) met carbon disclosure requirements within our model. While we’re encouraged by the level of initial participation, there’s clearly room improvement. To that point, we’re aware of several companies still the process of aggregating, auditing, and (eventually) disclosing relevant carbon data to investors, which should continue to improve the participation level in subsequent scorecards.

Superior Governance Translates To Outperformance:

• Companies with the strongest ESG scores (EGLE, INSW, ASC, TRTN, GNK, EURN, OSG, MATX, GRIN, GLOG, INT, GLNG, and KEX) outperformed the group by 16% on a 5-year basis and 41% since inception.

• Companies with the weakest ESG scores (CMRE, KNOP, TGP, CPLP, NMM, NNA, DSX, DLNG, GSL, DAC, TNP, GASS, and SB) underperformed the group by (24%) on a 3-year basis and (25%) since inception.

Read More

LNG Canada Update: Trouble Ahead For Shell’s LNG Flagship?

An Empty Module Yard & Mounting Schedule Delays

• Key Takeaways (pages 1, 5)

• Estimated LNG Canada Schedule Shifts (page 2-3)

• Satellite Image Review: COOEC Fluor Module Yard Layout (May 17, 2020) (page 4)

• Satellite Image Review: Module Layout Descriptions (page 5)

• Satellite Image Review: CFHI Module Yard Pre-Assembly Areas (page 6)

• Long-Term Thoughts & Key Questions (page 7)

Key Highlights:

• Still Moving At A Crawl. As of May, module fabrication was ~2% complete, well behind our ~11% estimate in W|EPC’s February 2020 (pre-COVID 19) schedule…

• Satellite Image Review: The COOEC-Fluor Heavy Industries (CFHI) module yard pre-assembly areas look…

• Playing Catch Up Won’t Be Cheap. The schedule slip should put even more pressure on the back-end of LNG Canada’s timeline…continued…

For access information please email us at [email protected]

Read More

W|EPC Risks: Venture Global – Keeping An Eye On Pile Design Changes

W|EPC Risks: Venture Global – Calcasieu Pass LNG – Keeping An Eye On Pile Design Changes

Key Takeaways:

• An engineering design change at Calcasieu Pass (CPLNG) required additional piling and out of sequence construction activities.

• Meaningful engineering changes during construction & fabrication can undermine the benefits of modularization, by creating cost overruns and delays.

• No Related Delays Are Visible Yet. However, we should get a better view of the actual impact as Calcasieu enters the mechanical phases of fabrication and construction – where the ramification of errors or changes becomes more evident.

Keeping An Eye Out For Material Quantity Growth. On May 22nd, 2020, CPLNG requested FERC approve eight (8) additional piles in the Pre-Treatment Common Pipe Rack 27X (PTC27X) area due to changes in the pipe stress data. Pipe stress calculations are developed to ensure the piping design and layout can support the expansions and contractions caused by processing hydrocarbons. Pipe stress data is one of the most important elementsin determining the piping layout, structural steel design, material quantities needed for the CPLNG modules, and pile layout.

The PTC27X pile construction design was previously submitted to FERC on December 30, 2019 and approved for construction on January 31, 2020. PTC27X piling submittal timeline:

• Original Submittal to FERC: 12/30/19

• FERC Approved: 1/31/20

• Revised Submittal to FERC: 5/22/20

• FERC Approved: 6/4/20

Was Module Engineering For PTC27X Finally Completed Last Month? On May 22, 2020 CPLNG requested FERC approve the PTC27X pipe rack foundations and steel construction. We believe the final PTC27X pipe rack module engineering is now complete, subject to FERC Approval. The PTC27X modules were designed per….continued

For access information, email us at [email protected]

Read More HL Acquisitions Corp. executes Business Combination Agreement with Fusion Welcome-Fuel, SA providing entry into the Green Hydrogen sector

Read More

EPC Risks: Energy Transfer (ET) Capital Project Monitor – Q220

W|EPC: Energy Transfer (ET) Capital Project Monitor – Q220

- Energy Transfer (ET) Q220 Capital Project Monitor: Key Takeaways (slide 2)

- Energy Transfer Capital Budget Overview (slide 3)

- Energy Transfer: NGL Fractionation History (slide 5)

- Tale of the Tape: ETvs. EPD (slide 6)

- Mariner East 2X (slide 8)

- Orbit Ethane Export Terminal(slide 9)

- Lone Star Express Pipeline (slide 11)

- Lake Charles LNG: Fighting Yesterday’s War? (slides 13-20)

Key Takeaways:

1. Does ET’s Frac 8 Have a Cost Advantage over EPD’s Frac 12?

2. Energy Transfer’s NGL BPD Frac Costs Keep Falling

3. Budget Cuts, COVID-19 Impact, & Schedule Delays

4. Lake Charles LNG – Fighting Yesterday’s War?

For access information, please email us at [email protected]

Read MoreSouthern Company (SO): Vogtle Nuclear Project Q220 Quarterly Monitor

Southern Company (SO) Q2 Vogtle Nuclear Project Monitor – Key Highlights:

• Vogtle Expansion: 6-Years Late…And ~$13-$16 Billion Over Budget? (Slides 2-5)

• How Much Will SO Be On The Hook For? (Slides 3-6)

• Something’s Gotta Give: Key Commissioning Milestones Appear Crammed Together To Avoid ROE Reductions (Slides 6-8)

• Cost Projections Were Already Ramping…Before COVID-19 (Slides 9-12)

• Cost Prudency Reviews – A Make Or Break For Stakeholders?…. (Slides 13-19)

For access information, please email us at [email protected]

- Quarterly Deep Dive Into Southern Company’s (SO) $27B Vogtle Nuclear Expansion. Southern Company (SO), is the largest owner of the Vogtle Nuclear Facility, via the 46% held by its wholly-owned subsidiary Georgia Power.

• Vogtle has two active units (Units 1-2), which have been in-service since 1987-89. A two unit expansion (Units 3-4) was approved in 2009

• Units 3 & 4 were originally expected to be in-service in 2016-17 and cost a combined ~$14B, the expansion project is now 6-7 years behind schedule, with costs rising to ~$27B….and potentially higher (slides 3-6).

• Hence, the premise of adding a W|EPC Quarterly Vogtle Project Monitor to our Utility & Energy research platform: Digging into those cost overruns – particularly the bulging EPC costs, to get a more accurate and detailed view of the potential headwind for project stakeholders and SO shareholders.

Regulatory Background: Vogtle is regulated by the Georgia Public Service Commission (GPSC). GPSC’s primary role is to protect rate payers & determine if project costs can be justifiably passed-through via utility rates. In the quarters that follow we’ll venture to aggregate, analyze, and interpret cost overruns through the lens of GPSC, to put together a thoughtful estimate of what cost overruns will eventually land with SO shareholders.

For access information, please email us at [email protected]

Read More

Webber R|A Renewables Weekly

Webber Research: Renewable Energy

Highlights:

- Orsted JV To Develop Clean Hydrogen In Copenhagen (page 1)

- US Extends Safe Harbor Deadlines (page 1)

- Next Generation EU (page 2)

- Saudi’s Alfanar Rumored To Be Senvion India Buyer (page 2)

- ENPH Collaboration With University of Washington (page 2)

- RUN Introduces Brightbox In Nevada & Colorado (page 2)

- ENS Board Changes & Dividend Declaration (page 2)

- SGRE SG 14-222 DD Backlog Updates (page 2)

- Vestas Expands 2020 Vietnam Intake To Over 300MW (page 3)

- Aerodyn To Develop 111-Meter TC1B Rotor Blade (page 3)

- US Net Electricity Generation (pages 3-4)

- Solar PV Pricing (page 4)

- LCOE Benchmarks & Timeseries (page 5)

- Global Wind Turbine Market Share (page 6)

- Solar PV Inverter Market Share (page 6)

- US Wind & Solar Projects Announced Or In Early Development (page 7)

Orsted JV To Develop Large-Scale Clean Hydrogen In Copenhagen: On 5/26 Orsted announced it entered into a JV with Copenhagen Airports, Maersk (marine), DSV Panalpina (logistics), DFDS (ferry), and SAS (aviation) to develop a hydrogen and e-fuel production facility. The project will be developed in three phases with the ultimate goal of providing renewable fuel sources for multiple transportation methods in the Greater Copenhagen Area. Phase 1 includes a 10MW electrolyser to generate renewable hydrogen fuel for buses and trucks – potentially operational as early as 2023. Phase 2 considers a 250MW electrolyser which would have the capacity to produce renewable methanol for maritime transport and renewable jet fuel for aviation – potentially operational by 2027 when the first offshore wind power is available from Ronne Banke off the island of Bornholm. Phase 3 would upgrade the electrolyser capacity to 1.3GW with the potential to displace 30% of fossil fuels used at Copenhagen Airports by 2030. Orsted said the project could reach FID as early as 2021 after receiving required regulatory approvals as well as a full feasibility study.

US Extends Safe Harbor Deadlines: continued…

For access information email us at [email protected]

Read More

Webber R|A Renewables Weekly

Renewable Energy Weekly

*REGI (Outperform) – Virtual NDR Weds 5/27 To participate email us directly or at [email protected]

Renewables – Weekly Highlights:

• GE To Add 193MW Onshore Wind In Turkey – Blades Built In-House (page 1)

• SPWR Sells O&M Business, Clears Maxeon Regulatory Hurdle (page 1)

• ENPH Expands Commercial Presence (page 1)

• IEA Updates Renewable Energy 2020 & 2021 Outlook (page 2)

• BNEF EV Outlook (page 2)

• AMRC Begins Commercial Operations In Ireland (page 2)

• SGRE Launches 14MW Direct Drive Offshore Turbine (page 2)

• Ginlong Solis To Double Manufacturing Capacity (page 3)

• Jinko & LONGi Launch New Modules (page 3)

• Sungrow To Provide Inverters For Ibri II Project In Oman (page 3)

• Suzlon Restructuring Update (page 3)

• PLUG Prices 2025 Convertible Notes (page 3)

• NJ Clean Energy Equity Act (page 3)

• US Net Electricity Generation (pages 4-5)

• Solar PV Pricing Dynamics (page 5)

• LCOE Benchmarks & Timeseries (page 6)

• Global Wind Turbine Market Share (page 7)

• Solar PV Inverter Market Share (page 7)

…continued

For more information on access and pricing, please email [email protected]

Read More

W|EPC: Objections To Venture Global’s Storage Tank Design

Venture Global – PHMSA Objects to Calcasieu Pass LNG’s Storage Tank Design

- A day after Venture Global successfully raised the first LNG storage tank roof

(4/27/20) at its Calcasieu Pass LNG facility, PHMSA issued a memo (4/25/20) to

FERC objecting to the LNG storage tank design, citing non-compliance with the

National Fire Protection Association (NFPA 59A). - LNG storage tanks must be designed and constructed to meet several regulations

and codes, including NFPA 59A. - The timing of PHMSA’s objection is notable since the tank design should

have been approved by PHMSA & FERC prior to the start of construction.

Continued….

Click here to buy this report

Webber Research: Renewable Energy Weekly

- ENPH Partners With 5B In Australia

- GE Renewable Energy Q1 Earnings

- Sunpower COVID Updates

- Safe Harbor Deadline Extension Brought To Treasury

- BNEF Semi-Annual LCOE Update (Page 2, Charts On Page 4)

- New York Approves Offshore Wind Plans, But Delays Action Due To COVID

- Orsted’s 120GW Skipjack Offshore Wind Farm Delayed 1 Year

- Q Cells Tops US Market Share

- Sunrun Hires New CFO

- Houston’s First Climate Action Plan

- California Confirms PV & Storage Installers Are Essential Workers

- Chicago Supporting EV Adoption

- Figures:

- US Net Electricity Generation By Type