client log-in

client log-in

W|EPC: Force Majeure & The LNG Supply Chain: Scenarios For BH, Kiewit, & Venture Global

Reviewing Satellite Images Of Italian Fabrication Yards & Force Majeure Flow Charts

• Supply Chain Overview Pages 1-2

• Satellite Images: BH’s Fabrication Yard In Avenza, Italy Pages 2-4

• Implications Of Calcasieu’s Unique Contractual/Structural Dynamics Pages 3-5

• Force Majeure Flow Charts: Wrapped vs Unwrapped Pages 4-5

• Pertinent Questions From Here Pages 5-6

For access information, please email us at [email protected]

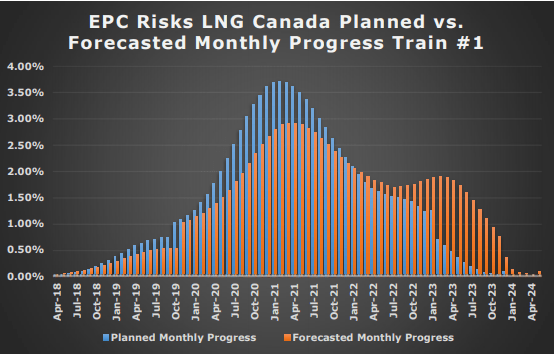

The LNG Supply Chain & Force Majeure Dominoes. Given the continued, rolling implications of the global response to COVID-19, we thought it was worthwhile to examine potential points of friction as it pertains to the implications of Force Majeure (FM) declarations on large-scale, multi-faceted LNG export projects. We believe such a scenario is relevant for Venture Global’s Calcasieu Pass (CPLNG) project given its globally linked supply chain – including its liquefaction modules which are being fabricated at a Baker Hughes (BH) fabrication facility in Avenza, Italy. (Satellite images on Pages 2-4)

Venture Global’s Potential FM Predicament Is Unique. A typical, fully wrapped, EPC contract would typically just keep an owner on the hook for extensions to a contractor’s guaranteed completion date. However, the less expensive, decentralized contracting structure that Venture Global has assembled for CPLNG could potentially expose the project to contractors looking to recover mitigation and prolongation costs. (Pages 2-4)

Implications Of FM Claim For BH, Kiewit, & VG. We believe work on CPLNG’s modules was still progressing last week (with non-essential personnel working from home), given the escalation in restrictions we believe those productivity dynamics are (justifiably) fluid. Should BH file a successful FM claim, it would most likely be granted… (Pages 3-6)

For access information, please email us at [email protected]

Read More