client log-in

client log-in

Webber Research: Fireside Chat Series – CoolCo LNG CEO Richard Tyrell, Thurs 9/28 @ 11am EST

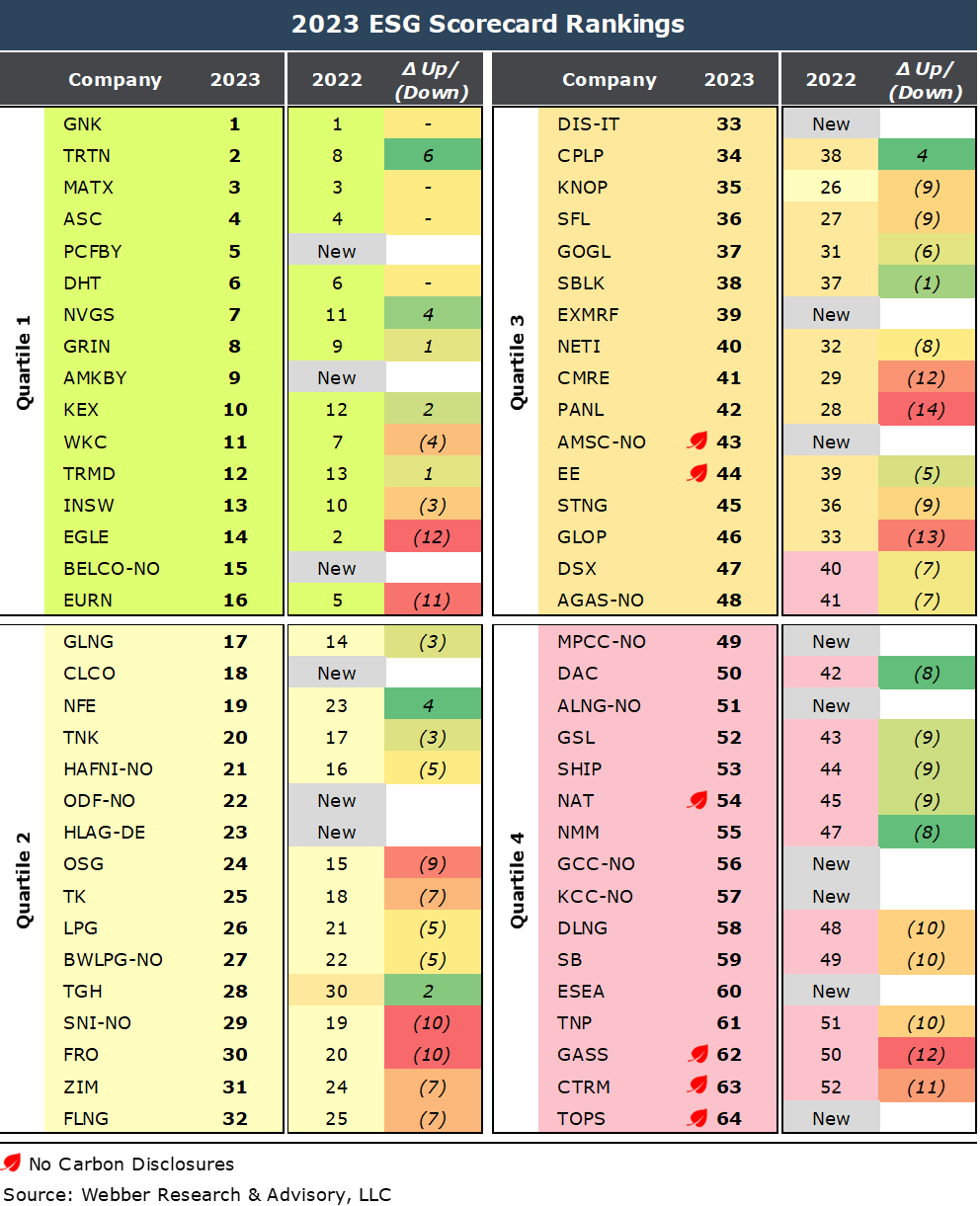

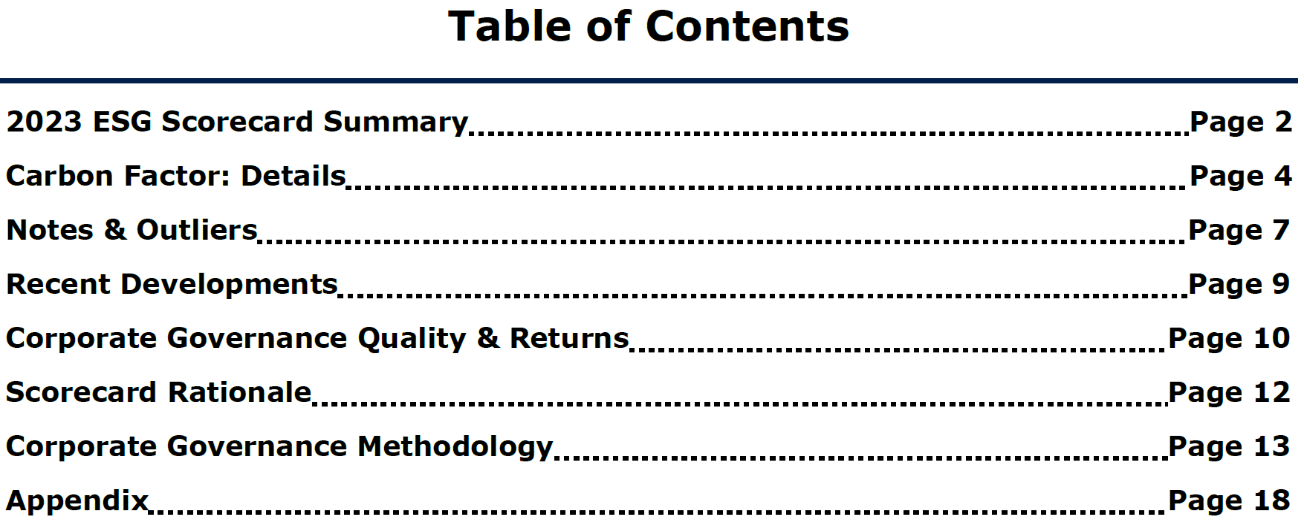

Webber Research: 2023 ESG Scorecard

If you’re a current Webber Research subscriber, you can click here to access this presentation in our library.

If you’re not yet a subscriber, please click here to download the full report, or email us at [email protected] for access information.

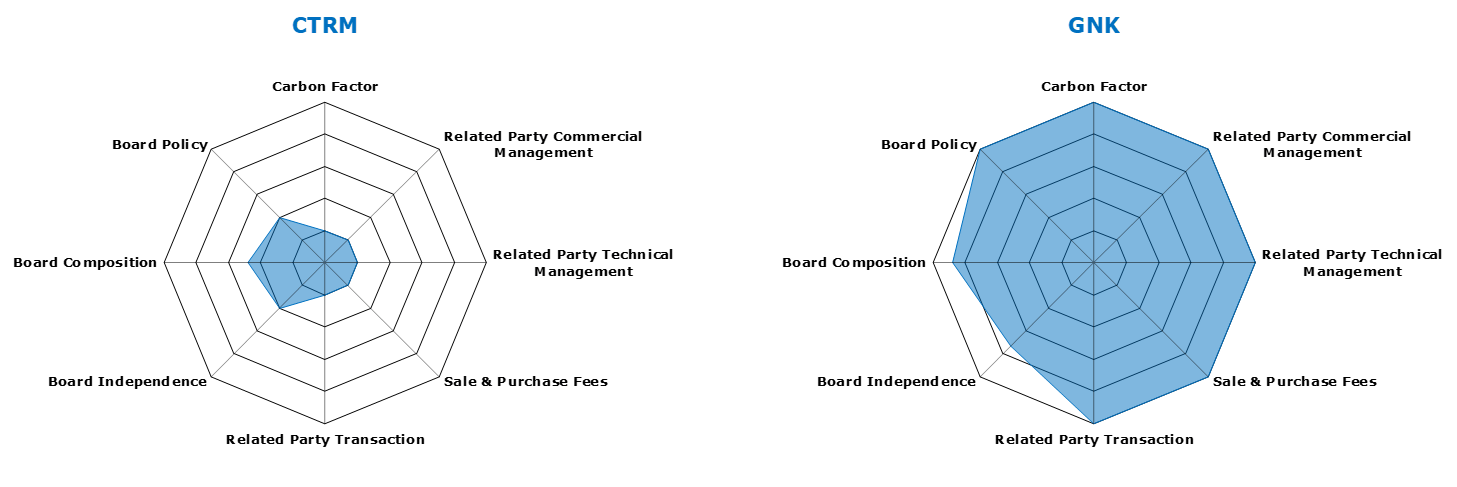

New for 2023: Company Specific Model Displays

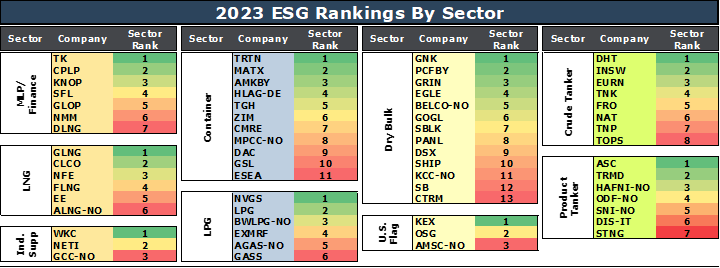

New for 2023: Sector Specific ESG Rankings

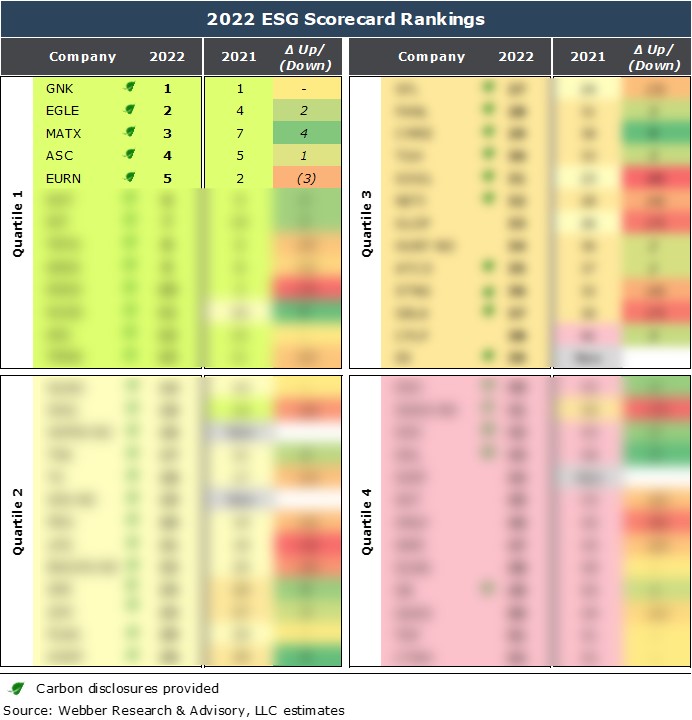

Webber Research: ESG Scorecard 2022

Access Full Report: Webber Research 2022 ESG Scorecard

Read More

Webber Research Fireside Chat Series – Kirby Corp (KEX) CEO David Grzebinski & CFO Raj Kumar – Weds, 5/4 @ 11AM EST

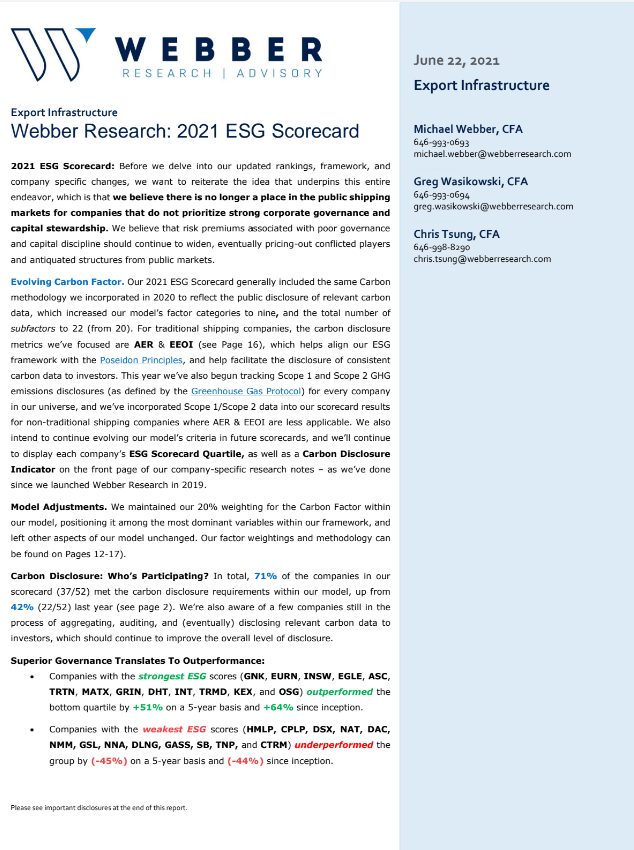

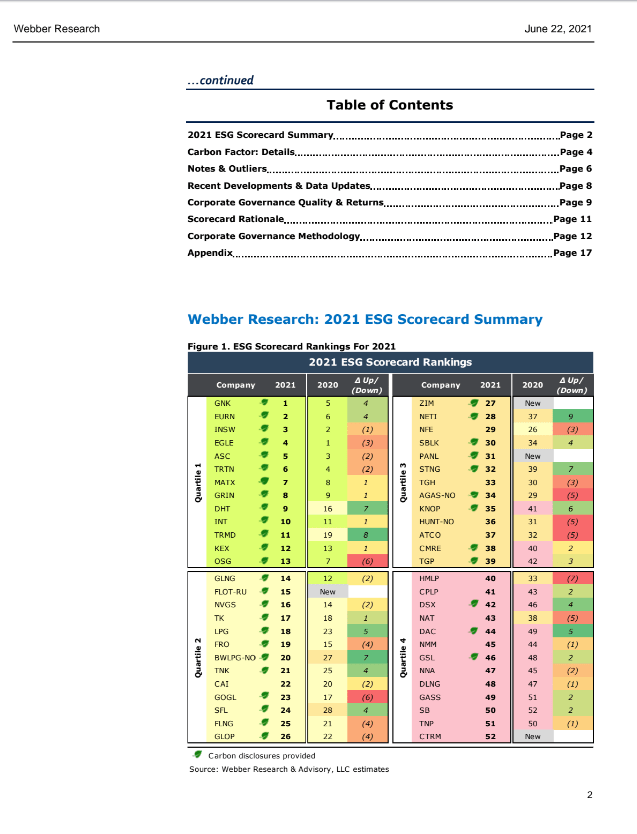

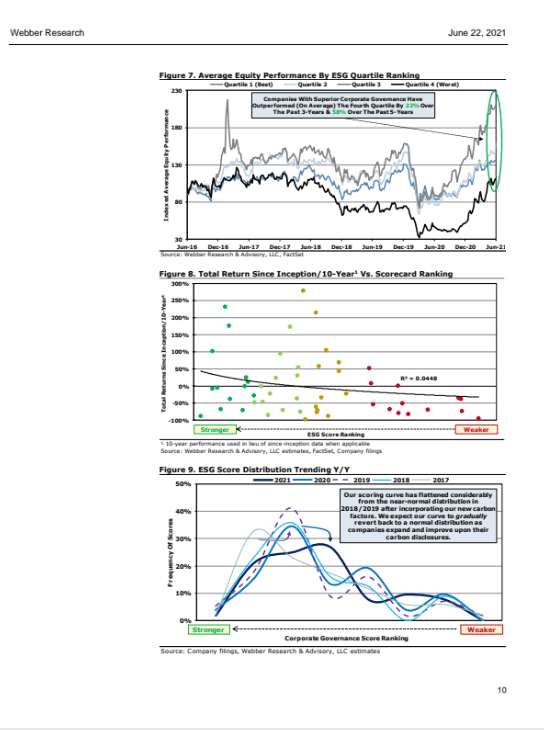

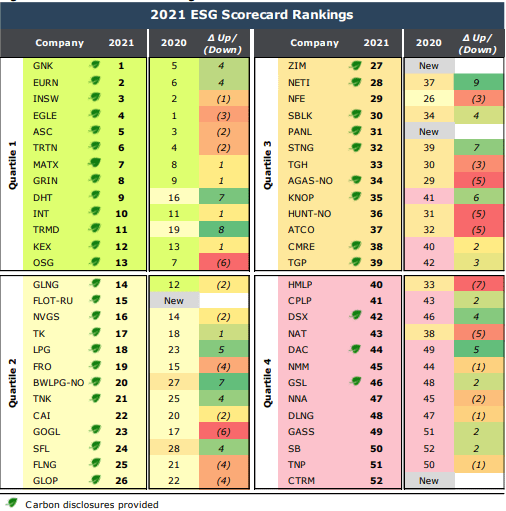

Webber Research: 2021 ESG Scorecard – Marine

Please contact us for a full copy of the report at [email protected]