client log-in

client log-in

Venture Global’s expanded 20-year contract a sign of revived LNG market as buyers avoid Russia

https://www.ft.com/content/064437a4-2c60-4962-b722-d669d71e914a

Read More

https://www.ft.com/content/064437a4-2c60-4962-b722-d669d71e914a

Read More

• Supply Chain Overview Pages 1-2

• Satellite Images: BH’s Fabrication Yard In Avenza, Italy Pages 2-4

• Implications Of Calcasieu’s Unique Contractual/Structural Dynamics Pages 3-5

• Force Majeure Flow Charts: Wrapped vs Unwrapped Pages 4-5

• Pertinent Questions From Here Pages 5-6

For access information, please email us at [email protected]

The LNG Supply Chain & Force Majeure Dominoes. Given the continued, rolling implications of the global response to COVID-19, we thought it was worthwhile to examine potential points of friction as it pertains to the implications of Force Majeure (FM) declarations on large-scale, multi-faceted LNG export projects. We believe such a scenario is relevant for Venture Global’s Calcasieu Pass (CPLNG) project given its globally linked supply chain – including its liquefaction modules which are being fabricated at a Baker Hughes (BH) fabrication facility in Avenza, Italy. (Satellite images on Pages 2-4)

Venture Global’s Potential FM Predicament Is Unique. A typical, fully wrapped, EPC contract would typically just keep an owner on the hook for extensions to a contractor’s guaranteed completion date. However, the less expensive, decentralized contracting structure that Venture Global has assembled for CPLNG could potentially expose the project to contractors looking to recover mitigation and prolongation costs. (Pages 2-4)

Implications Of FM Claim For BH, Kiewit, & VG. We believe work on CPLNG’s modules was still progressing last week (with non-essential personnel working from home), given the escalation in restrictions we believe those productivity dynamics are (justifiably) fluid. Should BH file a successful FM claim, it would most likely be granted… (Pages 3-6)

For access information, please email us at [email protected]

Read More

Tanker Spot Rates Soften Off Of Peak Levels As Saudi Reign In Freight Rebates: Spot rates weakened on slow fixture activity, crude prices bounding from under $25/barrel to ~$30/barrel (Brent), and Saudi Arabia announced limiting freight compensation to 10% of crude’s official selling price. According to TradeWinds, at least 10 VLCC & Suezmax spot fixtures loading Saudi crude had failed last week. VLCC spot rates (TCEs) led the decline with rates falling to $135.3K/day (-52% w/w and +408% m/m), Suezmax TCEs at $70.0K/day (-42% w/w and +166% m/m), and Aframax TCEs firming to $59.5K/day (+39% w/w and +120% m/m). We note rates remain well above consensus.

Roughly Half Of Bahri’s VLCC On Subject Destined For USG: Last week, Saudi Arabia’s Bahri put 25 VLCCs on subject after their announcement to flood the oil market (by increasing its production and lowering its oil price) in response to OPEC+ disbandment (see our OPEC+ Fallout note). VLCC rates had spiked as Saudi Arabia was said to provide freight rebates to some customers for crude transports between Saudi Arabia and Egypt. Bahri owns 41 VLCCs and rarely enters the spot market to charter third party tonnage. In addition to the large number of subjects, the intended destination for these vessels are telling of Saudi’s intent: 10 of the 25 VLCCs are destinated for the U.S. Gulf, 4 are likely going to Europe, 10 are fixed to discharge at the entry point of the Sumed pipeline (Ain Sokhna) which transports crude oil through Egypt to the Mediterranean (likely to end up in Europe). None of the spot VLCCs are fixed to Eastern destinations.

Scrubber Payback Period Upended Following Crash In Crude Prices: The spread between HSFO and LSFO has narrowed to $87/mt in Singapore and $47/mt in Rotterdam (Figures 2 & 3), extending the payback period to ~4 years. A VLCC fitted with a scrubber is able to command a spot earnings premium of ~$4.5K/day, down from nearly $20K/day at the start of the year.

For access information please email us at [email protected]

Read More

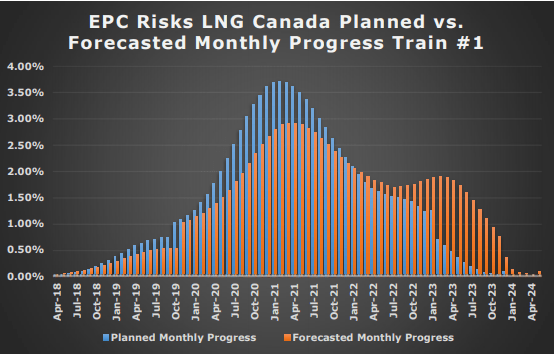

Update: In light of yesterday’s announcement that the Shell-led LNG Canada project was cutting its staffing levels in half over the coming days, we felt it worthwhile to pass along our LNG Canada Update from late February, along with a slide on our updated thoughts. (Page 2)

COVID-19 Impact Updates

1. The World Health Organization (WHO) officially declared COVID-19 a pandemic on 11-Mar-20.

a. JFJV may have a stronger FM claim now that WHO has declared the COVID-19 a pandemic, to the extent that JFJV specifically has “pandemic” or “epidemic” listed as an FM event in their contract.

b. FM Impact of Chinese module fabrication yards…….Page 4

2. On 17-Mar, LNG Canada and JFJV both announced that JFJV’s on-site workforce in Kitimat would be halved in order to increase social distancing and help prevent the spread of COVID-19. Given that the announcement was made jointly between JFJV and LNG Canada – impact on FM/schedule relief.…..Page 5

3.While JFJV did not announce when the site at Kitimat would resume a full workforce, it took “several” weeks for workers to return to JFJV’s Chinese fabrication yards…..Page 5

LNG Canada Planned Vs Foretasted Progress – Where Were We In February, and Where Are We Heading Now?…..Pages 5-8

Read More

***From Sunday 3/8***

For access information please email us at [email protected]

This Is Going To Hurt: On Friday (3/6) talks between OPEC and its OPEC+ allies (Russia) over a corona-related production cut collapsed, sending oil prices down with it (Brent and WTI down 9% and 10%, respectively on Friday). While the lack of OPEC+ support for crude prices was enough to rattle markets, what’s transpired since – the relationship between the Saudis and the Russians rapidly devolving into what looks like an all-out pricing war – has the potential to reshape energy markets for years to come, and will likely take the mantle as the most value-destructive policy shift in decades.

Exogenous Demand Shock, Meet Exogenous Supply Shock. As noted below, Aramco has already come out with discounted crude prices (OSPs) on the back of the meeting, and is reportedly speaking to a potential production ramp from its current 9.7mbd, to well above 10mbd, and could even reach a record of 12mbd. Again – that would be additional supply into a market that’s already oversupplied amid global efforts to contain the Coronavirus (nCoV) weighing on demand. While the Russians have less available swing production, what they do have will be moving in the wrong direction as well, as they look to grab share from U.S. Shale producers.

How Does This Impact Our Universe:

Tankers: We’ll Call It Mixed… (And That’s One Of The Few Bright Spots). Once the dust settles the tanker group, including FRO, DHT, EURN, ASC, etc, should be one of the few actual overproduction beneficiaries as: 1) tanker activity and rates are generally positively levered to production volumes (including overproduction), and 2) we expect to see floating storage, both economic (as the front end of the crude forward curve collapses (already in progress) and…….continued on Pages 3-5

Most Relevant Tanker Comp: 2015, after OPEC failed to respond to falling crude prices. While overcapacity and falling crude prices ravaged the rest of the energy markets, Crude Tanker rates (VLCCs) averaged $65K/day (Figure 4) – a level not reached since 2008, up 116% y/y and the firmest level in nearly a decade. What would 2015 day rates mean for current tanker stocks? If we replaced our current 2020 rate decks with the 2015 average rates….continued on page Pages 2-3

Everything Stops. If nCoV brought the near-term prospects of new LNG business to a particularly slow crawl, we believe the OPEC+ blow up will bring it to a full stop, at least until the dust settles. For companies in the process of restructuring (like TELL).….continued on Pages 2-3

For access please email us at [email protected]

Read More

|