client log-in

client log-in

Webber Research Expands Platform with Addition of LNG Industry Veteran Kamran Javed

Read More

Webber Research & Advisory Co-Founder Highlighted Among The 30 Leaders Driving Energy Transition In Shipping

Read More

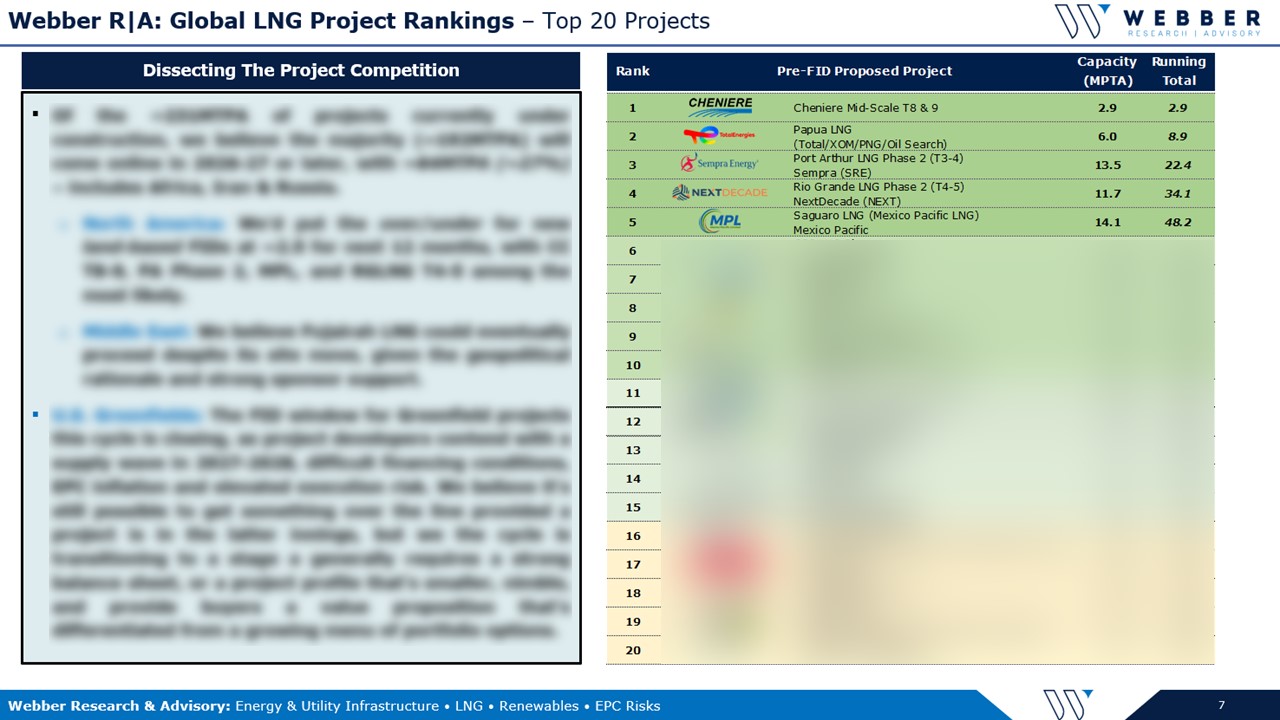

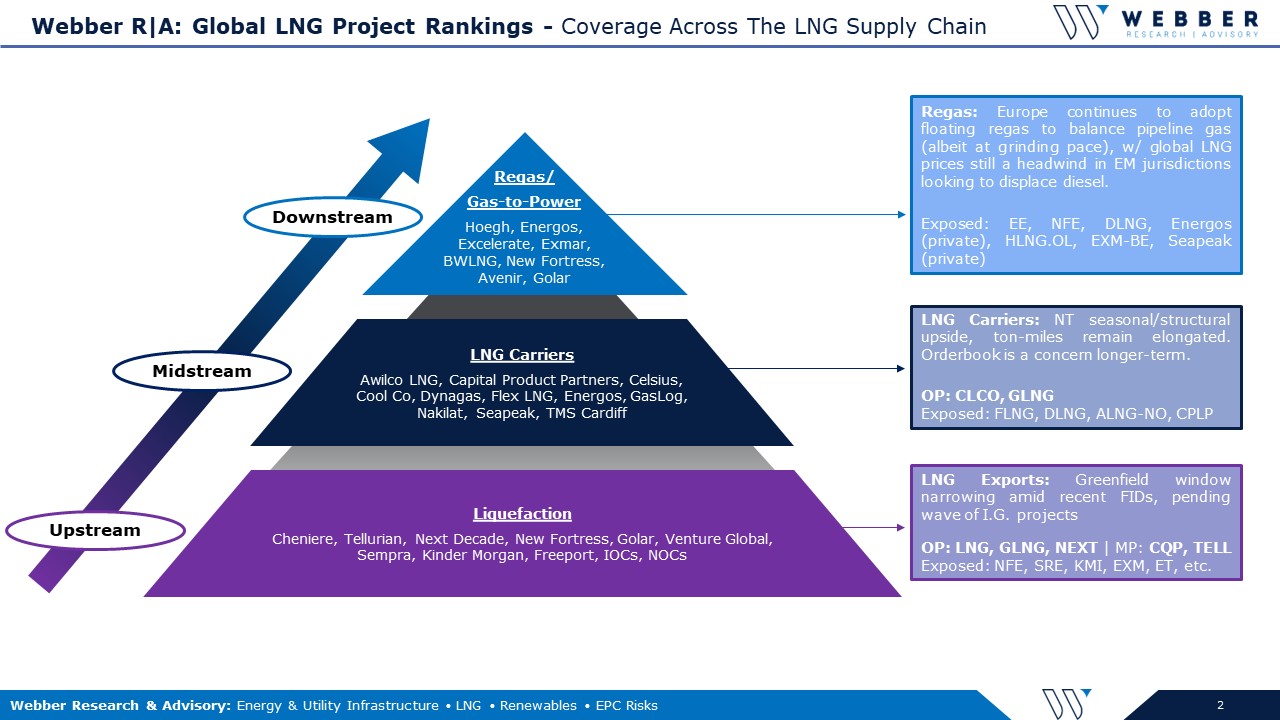

Webber Research: Global LNG Project Rankings & S/D Model Refresh – Q423

If you’re already a Webber Research subscriber, this report is available via our research library. For access information, email us at [email protected]. To download this report, click here.

Read More