client log-in

client log-in

W|EPC: Assessing Force Majeure Impact on Calcasieu (Venture Global), Golden Pass (Exxon, QP) & Sabine (Cheniere)

Webber Research – Energy EPC

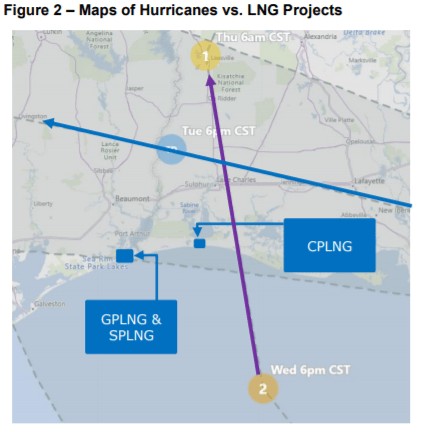

Marco & Laura Impact Could Last 7 to 14 Days…Depending on Damage & Craft Labor Retention

EPC contractors receive schedule relief for Force Majeure (FM) events (i.e. named storms such as Marco & Laura) in industry standard EPC contracts, which typically provides EPC contractors schedule relief but not cost relief.

EPC contractor FM claims on Calcasieu Pass, Golden Pass, and Sabine Pass LNG likely started yesterday August 24th, 2020 (due to mandatory evacuations & closures).

Something to watch…construction workers tend to scatter and chase higher paying (wages & per-diem) jobs post hurricanes/natural disasters, which creates headaches for on-going/planned projects and complicates FM claims.

Based on current Marco & Laura forecasts and expected rain/storm surge, we are forecasting a 7 to 14-day construction schedule delay on Calcasieu Pass LNG (CPLNG), Golden Pass LNG, & Sabine Pass LNG Train #6 (SPLNG6).

Impact & Timeline Implications

Often, impacts due to hurricanes occur well beyond the actual storm itself due to lost productivity and challenges restarting/staffing the project.

Flooding – enough drainage pumps installed and site drainage working sufficient to mitigate additional rain fall.

Storm Surge – levees/walls high enough to protect rising levels and all equipment moved to the highest elevation on the site (if practical).

Wind – cranes must be placed horizontally and structures secured to reduce/prevent damage.

Temporary Construction Facilities – if levees and/or drainage are not in place at temporary construction facilities, equipment and material stored in laydown yards/facilities could be damaged by water and cause unplanned long-term issues.

EPC contractors have a reputation for trying to use FM impacts to absorb existing self-inflicted schedule delays. Based on the current/expected forecast, we believe the following FM timeline is realistic.

Prep time for storms – 1 to 3 days

Marco & Laura storm duration – 2 to 4 days

Restart & productivity losses – 4 to 7 days

Our specific estimates and thoughts on individual projects in the pages that follow:

For subscription information, email us at [email protected]. For more information on this note, please visit our online store at webberresearch.com/downloads

Read More

OPEC+ Fallout: Contagion Everywhere From Looming Price War…

***From Sunday 3/8***

For access information please email us at [email protected]

Tankers Among Few Eventual Beneficiaries

- Impact On Tankers: Page 1, 3-5

- The 2015 Tanker Comp, Similarities, Implied Upside Pages 3-4

- Impact On LNG Developers (LNG, TELL, NEXT, GLNG, NFE) Pages 2-3

- Historical & Implied Equity Correlations To Crude Vol Page 3

- NAVs: Current, Mid-Cycle to Trough Range Page 3

- OPEC+ Background Page 3, 6

This Is Going To Hurt: On Friday (3/6) talks between OPEC and its OPEC+ allies (Russia) over a corona-related production cut collapsed, sending oil prices down with it (Brent and WTI down 9% and 10%, respectively on Friday). While the lack of OPEC+ support for crude prices was enough to rattle markets, what’s transpired since – the relationship between the Saudis and the Russians rapidly devolving into what looks like an all-out pricing war – has the potential to reshape energy markets for years to come, and will likely take the mantle as the most value-destructive policy shift in decades.

Exogenous Demand Shock, Meet Exogenous Supply Shock. As noted below, Aramco has already come out with discounted crude prices (OSPs) on the back of the meeting, and is reportedly speaking to a potential production ramp from its current 9.7mbd, to well above 10mbd, and could even reach a record of 12mbd. Again – that would be additional supply into a market that’s already oversupplied amid global efforts to contain the Coronavirus (nCoV) weighing on demand. While the Russians have less available swing production, what they do have will be moving in the wrong direction as well, as they look to grab share from U.S. Shale producers.

How Does This Impact Our Universe:

Tankers: We’ll Call It Mixed… (And That’s One Of The Few Bright Spots). Once the dust settles the tanker group, including FRO, DHT, EURN, ASC, etc, should be one of the few actual overproduction beneficiaries as: 1) tanker activity and rates are generally positively levered to production volumes (including overproduction), and 2) we expect to see floating storage, both economic (as the front end of the crude forward curve collapses (already in progress) and…….continued on Pages 3-5

Most Relevant Tanker Comp: 2015, after OPEC failed to respond to falling crude prices. While overcapacity and falling crude prices ravaged the rest of the energy markets, Crude Tanker rates (VLCCs) averaged $65K/day (Figure 4) – a level not reached since 2008, up 116% y/y and the firmest level in nearly a decade. What would 2015 day rates mean for current tanker stocks? If we replaced our current 2020 rate decks with the 2015 average rates….continued on page Pages 2-3

Everything Stops. If nCoV brought the near-term prospects of new LNG business to a particularly slow crawl, we believe the OPEC+ blow up will bring it to a full stop, at least until the dust settles. For companies in the process of restructuring (like TELL).….continued on Pages 2-3

For access please email us at [email protected]

Read More

LNG Update: Coronavirus Force Majeure — Context, Data, and Exposure

Corona-Related Force Majeure: Highlights From Our Recent LNG Update

- Chinese LNG Contractual Exposure – SPA Breakdown By Counterparty Pages 2, 5-9

- Historical Context – SARS, 6 Previous Global Health Emergencies Page 2

- NT Flash Points – 16 LNG Carriers Set To Call In China, Details Page 3

- Logistical Headwinds – Trucked LNG Data, Breakdown Pages 4-5

- Force Majeure Language – Cheniere (LNG) Pages 10-12

Coronavirus Puts Force Majeure In Play For Chinese Contracts: After days of speculation that Chinese LNG importers (CNOOC, Sinopec, CNPC) were considering invoking contractual force majeure clauses in their LNG contracts, CNOOC (China’s largest LNG importer – Figure 1) announced it had issued force majeure notices to their suppliers due to fallout from the coronavirus (nCoV). Total has reportedly rejected CNOOC’s notice of force majeure, setting up what we expect to be a continued string of notices and conflicting rhetoric, as the relatively opaque process plays out in a weakened and nervous LNG market, and amid the Q419 earnings cycle. While the ultimate impact of these contractual disputes is unclear – ranging from timeline delays (EPC), non-payment, and beyond — what does seem clear is that the issue should continue to build. As noted in Figure 3 – there are 16 LNG vessels scheduled to discharge in China over the next 5 business days, and we’d expect additional contractual flash points ahead.

Validity To Be Determined. We hope to get more clarity on the validity of force majeure claims in the coming days — particularly as they pertain to DES (fixed destination) and FOB cargos (flexible destinations — like Cheniere’s) which can be diverted to unaffected markets. We would think it’s less likely Cheniere’s FOB cargoes would be impacted by force majeure issues at the geographical origin of the original purchaser, given their inherent flexibility.

More Than Just A Demand Headwind In China. It’s also worth noting that Corona issues go beyond simply demand destruction within the Chinese market. Given pipeline infrastructure limitations in China, significant volumes of LNG are trucked to end users (Figures 4 & 5), which also brings logistical issues to the forefront, as there’s likely a similar lag in LNG truck drivers returning to work as those in factories and mills following the Lunar New Year holiday and quarantine efforts by the Chinese government. The risks also expand beyond volume-based LNG contracts, with shipyards, hard-asset delay schedules and tangential energy infrastructure also potentially impacted. Late yesterday gas producer Energean noted TechnipFMC had claimed corona-related force majeure on a FPSO meant for an Israeli offshore project

For access information, email us at [email protected]

Read More

LNG Update: USG Pricing Color & Mubadala Builds Its NEXT Stake

Updated Pricing Color For U.S. Developers: Cheniere, Shell, Venture Global, Next Decade, Freeport, Annova, Commonwealth, Delfin & More. Over the past week we’ve had several conversations with LNG buyers, project developers, and downstream operators, with the more pertinent color below:

LNG Pricing Currently Being Offered In The USG:

• Consensus Range: $2.25–2.40/mmbtu – Individual Developer Pricing Details On Page 2

• Outlier: $2.10-2.20/mmbtu – Individual Developer Pricing Details On Page 2

• Outlier: Offering ~$1.75/mmbtu – Individual Developer Pricing Details On Page 2

Favored Projects: Buyer With Some Effective Baseload Exposure – In the U.S. only really considering a handful of projects (page 2), however, Qatar is the most likely – and buyer has option to pull from Ras Laffan or Golden Pass. Webber Note: the optionality here provides another window into how Qatar is marketing their entire ~100mtpa portfolio.

Venture Global: At least 2 buyers in Calcasieu potentially going back for more LNG in Plaquemines, site visits are still ongoing (page 3).

Project Roll Ups: One buyer speculated we’ll see some of the 3rd and 4th tier Greenfield projects get rolled up in 2020, as existing players look for cheaper growth optionality and early stage projects solve for funding issues. Webber Note: we agree, and think it could start in the next quarter or two, with a Brownfield or well-funded player consolidating some pre-FEED or pre-FERC powerpoint projects.

Mubadala Builds NEXT Equity Position: On 12/12, NEXT filed a shelf registration for 10.1MM shares, controlled by Mubadala Investment Company (Mubadala) – 8.0MM of which were issued to Mubadala on 10/24 (at $6.27/share) and 2.1MM of which Mubadala acquired from another shareholder (we believe BKR). While the stock traded off 4% as the registration headlines spooked the market a bit (unfortunately, a relatively predictable outcome, even for a maintenance filing), the stock regained the lost ground relatively quickly. We view the BKR sale (via BHGE) as mostly a post-spin cleanup effort, with at least read through here that Mubadala likely wanted more equity than NEXT was willing to issue on a primary basis.

For access information, please email us at: [email protected]

Read More