client log-in

client log-in

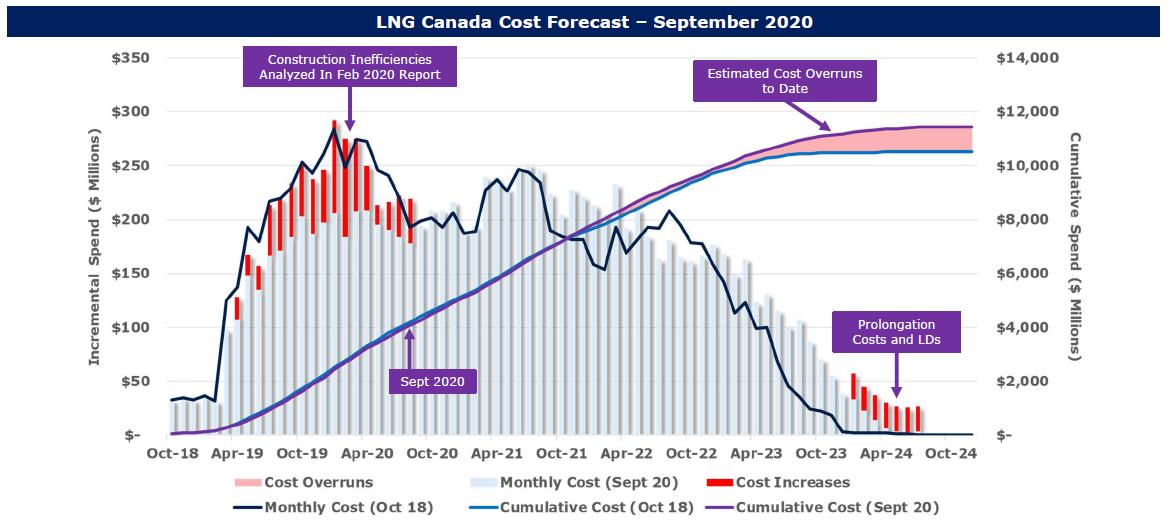

W|EPC: Southern Company (SO) – Q420 Vogtle Project Monitor – Key Decisions That Could Haunt Cost Prudency

Key Takeaways: Vogtle Q420 Monitor – Key Decisions That Could Haunt Cost Prudency

Who Will Be Getting Stuck With +$2.1B In Cost Overruns? Once Vogtle Unit 4 reaches “fuel load”, Georgia Power/Southern Company (GP/SO) can request a cost prudency determination to push their portion of cost overruns (~$2.1B) into recoverable utility rates. (Page 4)

Regulators will determine cost prudency based on project data, testimony, and a simple question: What should a reasonable manager have done at the time of the decision? (Page 5)

We expect that process to be heavily scrutinized considering the scale of the overruns, and, in our opinion, some questionable GP/SO decisions. (Pages 4-5)

Decisions That Could Haunt GP/SO’s Prudency. We believe there’s a case to be made that multiple GP/SO management decisions ran contrary to industry standards, potentially contributing to ($) billions in cost overruns, including

- A failure to either include or implement multiple EPC contract……(Page 7)

- For the first 4-years of the project, GP/SO used only…..(Page 23)

- In 2017, it appears GP/SO did not validate critical underlying EPC…..(Pages 9- 10)

Analyzing 12-Years Of GP & SO Testimony… (Pages 20 & 23)

Please join us for our next Client Call at 12pm EST on Monday 10/26, to review our Vogtle Project Monitor. Please reach out to us for access details.

![]()

Table Of Contents:

- Key Takeaways – Page 2

- Who Owns $2.1B In Cost Overruns? – Page 3

- Georgia Public Service Commission 2018 Order – Page 4

- Cost Prudency Definition & Process – Page 5

- Decisions That Could Haunt GP/SO

- LSTK Contract Mismanagement – Page 7

- Bankruptcy – Parent Company Guarantee Settlement – Page 8

- Estimate to Complete – Page 9

- Transition from EPC LSTK to T&M – Page 10

- QRA – Cost – Page 11

- QRA – Schedule – Page 12

- GP Testimony & W|EPC Analysis (2009 to 2017

- EPC Contract Overview – Page 14

- October 2009 – Page 15

- October 2010 – Page 16

- April 2011 – Page 17

- November 2012 – Page 18

- June 2013 – Page 19

- October 2014 – Page 20

- October 2015 – Page 21

- December 2015 – Settlement of LD’s – Page 22

- December 2015 – Revised EPC Contract – Page 23

- October 2016 – Page 25

- April 2017 – Page 26

For access information, please email us at [email protected], or our institutional sales at [email protected]

Read More