client log-in

client log-in

Webber Research: 2024 Shipping ESG Scorecard

To view our full report, visit our Downloads page. If you’re already a Webber Research subscriber, visit our Library. For access information, contact us at [email protected], or at [email protected]

Read More

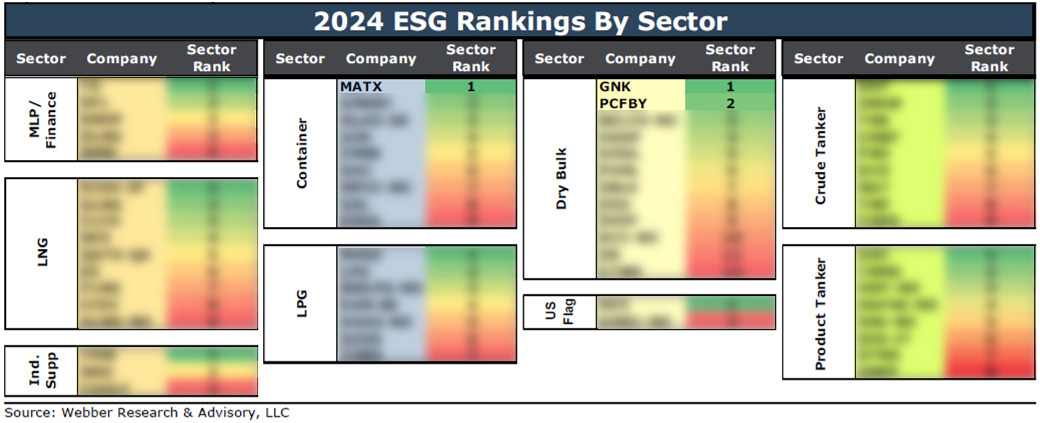

Tradewinds: Webber Research’s 2024 ESG Scorecard – Genco reigns, CMB.Tech tumbles and Imperial Petroleum lags

Read More Webber Research & Advisory Expands LNG & Energy Infrastructure Platform With Addition Of LNG Industry Veteran Alexander Bidwell

Read More